One of the most important paradigm shifts of 2023 will likely be how Artificial intelligence (more specifically ChatGPT) invaded our lives and captured the zeitgeist of not just the world but also an entire generation. It stamped itself as a technological force of change that promises to alter our lives forever. Like several technological revolutions that preceded it, humanity and corporations will be quick to acknowledge it as a change agent, but its absorption into everyday lives and workflows could take time.

It must be expected that the companies at the forefront of such “disruptive” technologies will capture the imagination of the hoi polloi and the investing herds on Wall Street and elsewhere in the financial world. NVidia has become the de facto flag-bearer of this revolution. On the other hand, companies which are perceived to be at the receiving end of such dramatic and disruptive technological changes have overnight become near pariahs on Wall Street as investors, turning fearful, are already ringing the death knell for this set of companies and businesses.

As is usual, there are fundamental truths to such an epochal change, but there is also plenty of hype and hyperbole that accompany them. It is a good time now to pause, take a deep breath and assess both sides of this unfolding parable.

Think of the changes wrought by the LAN/WAN and the networking revolution, PCs, email, the World Wide Web, Apple and its ‘i’ products, ERP, Cloud, SAAS and, more recently, the Metaverse. It is true that some technological changes have indeed brought about the death of some companies along the way, but it is equally true that as many or more have survived by adapting themselves and morphing into very different creatures. Names such as Motorola, IBM, Cisco Systems, eBay, Oracle, Xerox, Blackberry, HP and many more are still around and continue to chart their own destiny in a new world.

Perceptions being created today are typical of what happens when a new-fangled technology catches the imagination of the masses. Shrewd investors ought to be able to distinguish reality from the perception and not be entrapped in the chimera. As investors, this is a time for us to be on ‘high alert’ to such changes happening in the world around us – to rethink entrenched postures, to reimagine the future and remodel portfolios to be the proverbial early bird that catches the worm. It would also pay to take note of the market’s early exuberances and apathy, both of which are throwing up unexpected opportunities.

The Arrival Of Artificial Intelligence

We are at an epochal moment in the history of technological change when Artificial Intelligence has advanced to a point where it is ready to be applied and assimilated and make a meaningful change in our everyday lives. The advent of ChatGPT and Generative AI is perhaps the most profound of technological breakthroughs we have seen in decades.

Knowing what we do not know is often more important than what we already know. We know that AI is going to make a profound impact on economies and, by extension, markets and us as investors in future. The sheer possibilities of the applications and use cases are enough to shake up the existing citadels of several industries and companies. What is highly uncertain though is by when and how AI would begin to matter and become tangibly impactful for the global economy.

Like everything else that preceded AI, it comes with its share of challenges, high bars and walls to tear down. Large language model (LLM) technology is still evolving. Its impact today is greatest in small sub-segments of the global economy. This makes it difficult to extract and estimate its true impact on growth statistics.

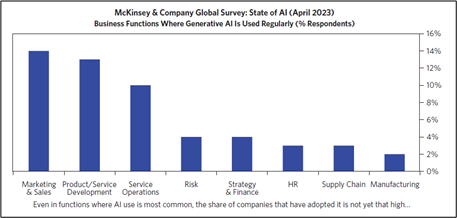

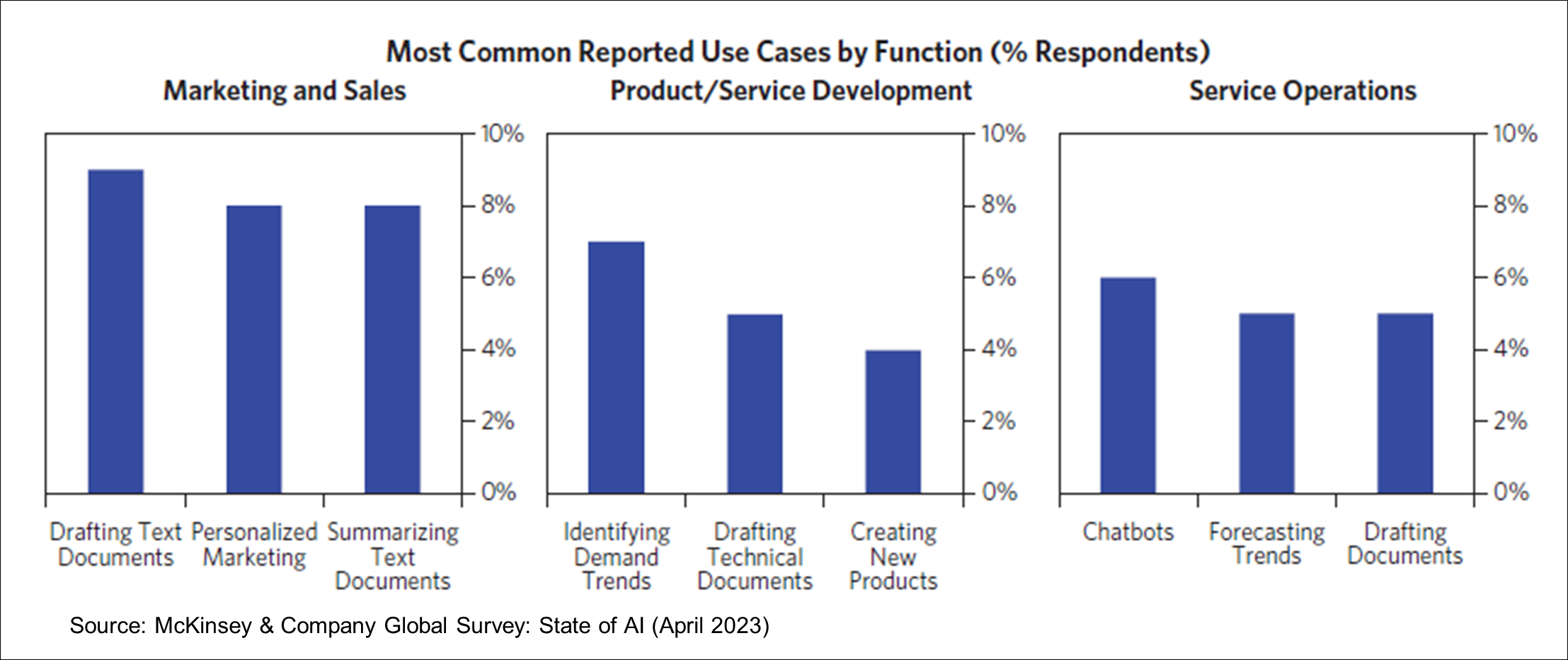

Usage is likely to broaden but at the beginning the impact is likely to be concentrated in a handful of industries, more so at the sub-segment level. LLMs are particularly suited for integration into workflows that are based on text in a constrained environment (i.e. where text or speech follow consistent patterns). It is being assimilated quickly in functions that meet such criteria. Also, these areas are where downsides or risks arising from, say, lack of precision or a murky regulatory set-up are less acute.

We are seeing early experimentation with generative AI tools across a wide variety of tasks but not many areas where the use of the technology is widespread. The best guess is that generative AI tools will eventually be meaningful productivity enhancers across many work streams. However, the most important takeaway is that this process is in its infancy. Companies are still figuring out the technology, trying to work out its best use for their businesses and the areas where it can be applied with meaningful cost and efficiency impact. They are also assessing the regulatory impact and the current landscape while preparing for its adoption.

A McKinsey & Company survey conducted in April 2023 found that around one-third of respondents’ companies had begun the use of generative AI in at least one business area. They also found that companies were experimenting across a wide range of use cases, with no single area or use case seeing widespread adoption thus far.

Impact Of AI Possibly Still Many Years Away

Most studies of AI adoption forecast that the major productivity impact will occur in the 2030’s or 2040’s, most likely not in the next few years. These estimates are largely based on past experience of productivity changes. There tends to be a long lag between invention and macroeconomic impact. Most commercial uses of technologies require other inventions to happen side by side, which begin to develop over time. For example, the invention of the spreadsheet, or database management systems, etc., gave a totally new dimension to the utility of PCs.

Companies need to create tools and techniques to incorporate these new AI technologies into workflows which will, in turn, require retraining people to use them effectively. This means that, for many companies the cost of investing in such technologies will come ahead of the actual benefits arising from their use. The primary benefits of general-purpose technologies typically do not come from doing the same processes faster but rather from totally new approaches that they enable. Once again, getting this done is going to take a lot more time than is currently believed.

While history need not always repeat itself, some estimates of AI adoption from a few years ago look naively optimistic today. A 2019 study from the MIT Technology Review had concluded that 12% of all jobs in Asia would be automated by AI by 2024. Another 2017 study by PwC had forecast that across most industries between 50-90% of potential AI use cases would already be implemented by 2023. Thus we believe that the adoption of AI will likely flow through to productivity faster than past general-use technologies, but its full impact is likely to still be many years away.

As in the past, there is no dearth of studies that have been conducted which make similar projections and forecasts. The methodologies used in such studies is often imprecise. Broad definitions of tasks only loosely correlate to what jobs actually require and AI’s ability to perform a certain type of task does not mean that it can do it in the way that such jobs are required to be done. This makes these estimates very sensitive to assumptions and human judgement errors of under- or over-estimation.

Hyperbole and Narrative Clashing With Stark Realities

In the excitement of the possibilities of what AI can do, investors seem to be caught up in the hyperbole and narrative and are setting themselves up for disappointment in the short to medium term, since the actual outcomes of AI adoption may fall far below their elevated expectations and could take much longer than their current investment frameworks allow room for.

Most notably, customer contact centres and software development are the two industry sectors which have most fallen prey to this hyperbole. Of course, there are compelling cases to integrate AI here. Customer contact mostly involves routine inquiries about basic information and is often voice- or text-based, making LLMs a good fit. The desire to reduce labour costs is high and, since labour is a very large share of total costs in the industry, it is an area where adoption could come early.

How efficacious can AI be? Data availability is limited right now as we are still in the early stages of understanding and adoption of these technologies. However, a recent study of a company that implemented a particular AI tool to prompt technical chat support agents found an increase in issue resolution per hour by 14%, while a recent survey found that using AI tools to assist agents during contacts reduced average handle time by 27%. These tools so far have been used more to assist rather than replace existing agents, by prompting agents or handling note-taking tasks. The survey suggests that it is possible that, in future, the use of AI tools could lead to not just an absolute reduction in headcount but also the increase in output delivered from the use of such tools.

For IT Services companies, the impact is likely to be first felt in areas of marketing automation, testing and documentation. Many of these service lines are traditional ones whose share of total revenues for companies today has become very small anecdotally (companies have stopped providing granular break-up of revenues). Either companies providing these services will be quick to apply AI tools in these lines to defend the business or, even if they were to allow it to atrophy away, it is expected to do so over time when other offsets are likely to be found. Hence, it is very difficult to ascertain at a sector or company level the precise negative financial impact that AI will have.

Industry has been quick to respond: In the IT Services sector, especially in India, almost every company is gearing up investments in the area of Generative AI, including partnerships with ecosystem players (such as hyperscalers) and academia, training employees and, in some cases, even building their own LLMs and industry solutions.

Take TCS as an example. TCS has products such as Ignio, Optumera, ADD, and TwinX, which use AI and ML to transform their respective focus domains. It has launched a Generative AI Enterprise Adoption offering on Microsoft Cloud to help customers jumpstart their Generative AI journey. TCS claims to have trained 50,000 employees in AI/ML solution-building skills, with over 9,000 having top external certifications. It plans to create a talent pool of over 100,000 Generative AI-trained associates and intends to get 25,000 associates certified on Azure Open AI by 2025-26. Over 50 proofs of concept and pilots have been created. TCS says it has more than a hundred opportunities in the pipeline that will be monetized over time. Multiple teams in almost every vertical that TCS has are working on pilots and internal projects. TCS has filed over 710 patents for AI inventions in the past five years of which 282 have been granted so far. TCS has launched an advisory offering to help clients create a holistic vision, strategy and plan for enterprise-wide adoption of Generative AI.

Accenture (ACN) noted recently post its 3Q23 results that it has planned investments of USD3bn over the next three years. ACN noted that Generative AI can help the industry with improved productivity, particularly in system integration and consulting, as the IT industry’s business model requires at least 10% productivity gains every year. Generative AI is currently being used more in documentation and very little in complex transformation projects at enterprises. ACN expects its adoption to be faster than cloud adoption, which took a decade.

Companies generally believe that the early and higher value capture in the Generative AI cycle would be done by hardware suppliers (e.g. NVIDIA) and software companies (e.g. cloud hyper scalers). Yet, investors are curious about the initial use cases of Generative AI and its possible deflationary impact on IT services companies. There is equal curiosity to fathom if there are bigger business opportunities for IT services companies in the long term despite its possible deflationary impact on their revenues. From the commentary by various Indian IT services companies thus far, it is apparent that the preparedness to ride the demand wave in Generative AI is much higher than the cloud cycle, as evidenced in the recent announcements of ecosystem partnerships and employee training.

Challenges are several, real and far from resolved: The biggest challenges which remain yet unresolved are issues around privacy, governance and, most importantly, costs. There are still significant hurdles to overcome – data privacy, security and IP are the biggest challenges for AI implementation. Data will be the prized asset in differentiating AI models. Expect to hear about large conflicts as enterprises seek to collect, safeguard and monetize their proprietary data.

Many believe that while Generative AI is likely to significantly increase the use of automation and therefore be deflationary for contact centres/BPOs and testing initially, it is likely to increase the volume of work overall, as enterprises would need to standardize their data and increase their cloud adoption to harness the Generative AI technology.

Impact On The IT Services Sector As Stocks React

Over the last three or four quarters, IT services companies have been caught in a perfect storm. Coming into 2023, the sector sat uncomfortably on a very high comparable reporting period of revenue and profits arising from the effects of the pandemic. These were beginning to wear off. At the same time, the arrival on the scene of ChatGPT and Generative AI has made a massive impact on the stock prices in this sector, due to some of the following:

- User industries and CTOs are being forced to slam the brakes on signing off on new deals/projects until Generative AI et al were well understood. Delays in decision-making have lengthened sales cycles and lowered revenue visibility;

- As global demand slowed down post the pandemic coming into 2023, discretionary spends in IT services also began to come off sharply. TCS and Infosys, who reported their Sept’23 quarter results recently, made direct reference to this as a key reason for their lower revenue guidance for the rest of the year; and

- Global companies operating in the Customer Experience or CX segment of BPOs (which in itself is a US$90bn service category globally), are seeing a sharp deceleration in demand from early 2023 itself, especially from certain clients like Meta, Amazon, etc. These companies saw a surge in demand during the pandemic but are now backing away from such spending, thus impacting the revenues of the CX segment.

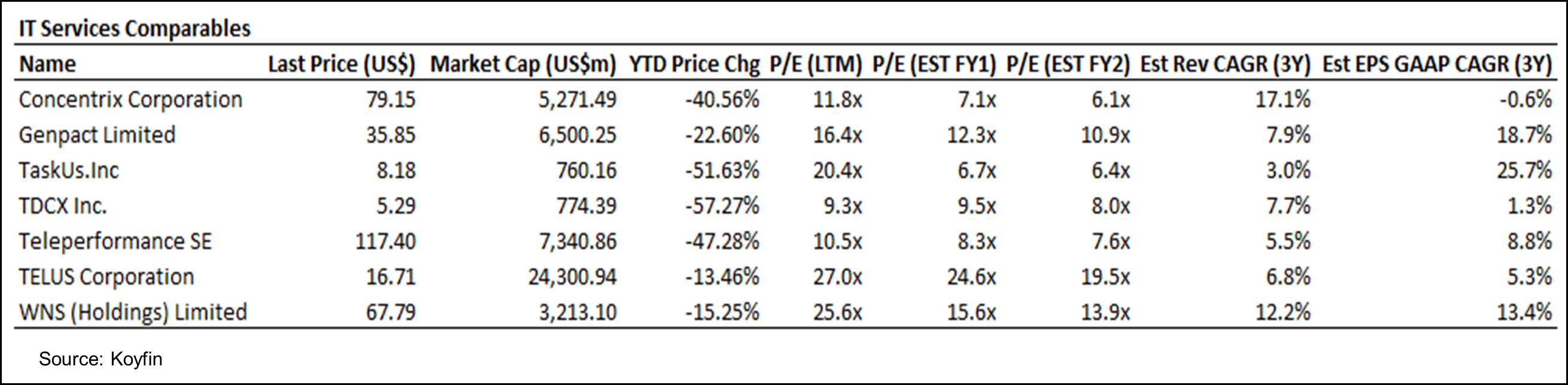

Management commentary coming out of industry leaders like Teleperformance and Concentrix as well as smaller competitors like TDCX, TaskUs and Telus echoes the same refrain. Their guidance cuts came at a time when the excitement surrounding ChatGPT and advent of Generative AI captured the imagination of a generation of users. This caught the IT services companies like the proverbial deer in the headlights of investors. Result: large earnings cuts across the board, followed by the expected de-rating of their stock valuations to multi-year lows.

Industry and investors will now have to wait for early CY24 when new growth forecasts and targets are spelt out, to get more visibility and confidence on the demand outlook.

The CX-based BPOs’ stock prices globally have been hammered. Stock prices are factoring in deep disruptions in the business performance of these companies over the next three to five years. Clearly, many believe these businesses have either turned ex-growth or that they could be totally disrupted.

The jury is out but it must be said in their defence that these companies have traversed many technological transitions and adapted and morphed along the way and thrived. The industry is a lot more consolidated today and will be even more so once the few large M&As in the works are completed. This sector generates solid and stable cash flows and has given good payouts to shareholders.

A CX company we spoke to and some industry professionals we have been speaking to say that the industry is cognizant of the challenge that Generative AI presents and is already at work to find ways to incorporate it into their systems and workflows so as to offer AI-based solutions to the same clients in future without being disrupted. They believe that while some low-end work could well be in-sourced by companies themselves, much of the outsourced work will continue to be outsourced as corporations do not wish to be investing precious dollars and manpower in ancillary tasks and would rather focus on their core skills, be it manufacturing, marketing or branding. CX companies will buy AI tools and apply them to provide the same services perhaps in a more efficient manner with a smaller workforce but where volume and price will have to find an equilibrium. It is still uncertain whether this transition is going to be as deflationary as it is made out to be and in what parts of the business. Data integrity and ownership and security issues are major sticking points and corporations will not be easily persuaded to make any compromises there anytime soon. Companies will also need a lot of convincing that AI tools will make a tangible difference to costs and output for them. This is far from certain and will take a lot of time and doing to achieve at global scale.

To conclude, the de-rating of IT services companies’ stock prices today is a function of multiple factors coming together at the same time – weaker growth guidance leading to lower reported growth in 2023, lowered multiples arising from the higher interest rate environment globally and the perceived risks of Generative AI impacting their long term business prospects being over-compensated in their NPVs being marked down dramatically.

Risks And Opportunities In The Sector

The risk is that this trend persists for some time as global corporations take longer to assess the adoption of the technology. This has and could lead to further delays in decision-making. Some believe that the scope of some projects could change and pricing, which has held up well thus far, could come under the scanner. But this could be compensated by a larger volume of work (pent-up and forward demand). The net impact could be neutral to mildly negative, depending on which vertical companies are more exposed to. A higher willingness to try AI is visible in companies in the BFSI, retail, hi-tech and life sciences sectors. Companies having higher exposure to these could potentially be worse off.

Given that companies in this sector have a long history of adapting and surviving through the most trying of times, it is more than likely that they will figure this one out too before long and the strongest among them could come out stronger yet. We note that investors had voiced similar apprehensions a decade or more ago when cloud appeared on the scene, but which were belied quickly when they realized that the transition to the cloud was not as disruptive to their well-being as was imagined.

Investors’ trepidations are valid and well understood. They might seek a greater margin of safety given the uncertainties and lowered visibility of earnings in the short term. But as the shroud of mystery lifts and the clouds of uncertainty begin to clear, the sector ought to revert back to trend growth.

The current dislocation in pockets of the market, especially the BPOs and CX companies, presents an opportunity to assess the sector and stock level risks and pick long term winners, as there surely and inevitably are some at such turning points in history.

Anti-Obesity Pills – Creating Value Elsewhere

Another disruptive change happening is in the field of healthcare where Eli Lily and Novo Nordisk are on the cusp of raking in tens of billions of dollars a year hawking their anti-obesity drugs known as GLP-1 receptor agonists, which promise body weight reduction of up to 20%. By all counts they are possibly the safest solutions to this age old malaise that afflicts millions of people all over the world. Wall Street has been cheering the stocks of these companies for some time now, taking them to valuations that are beyond comprehension on conventional wisdom and metrics.

What has got less attention from investors is that they could trigger a crisis in the healthcare sector as the huge spending on these drugs threatens to overwhelm the insurers, employers and government agencies that buy these drugs. The strain of paying for the drugs could cascade into a systemic problem that many are now waking up to.

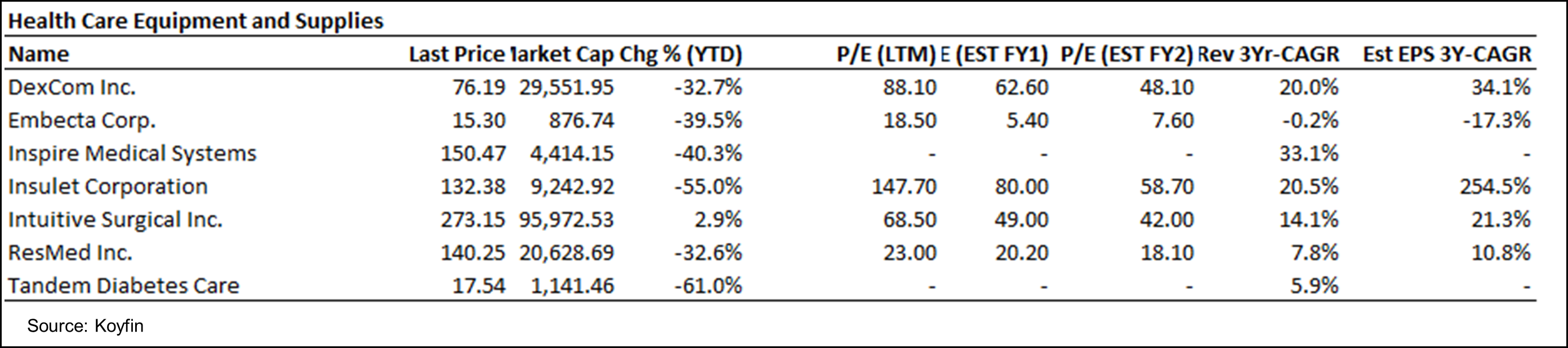

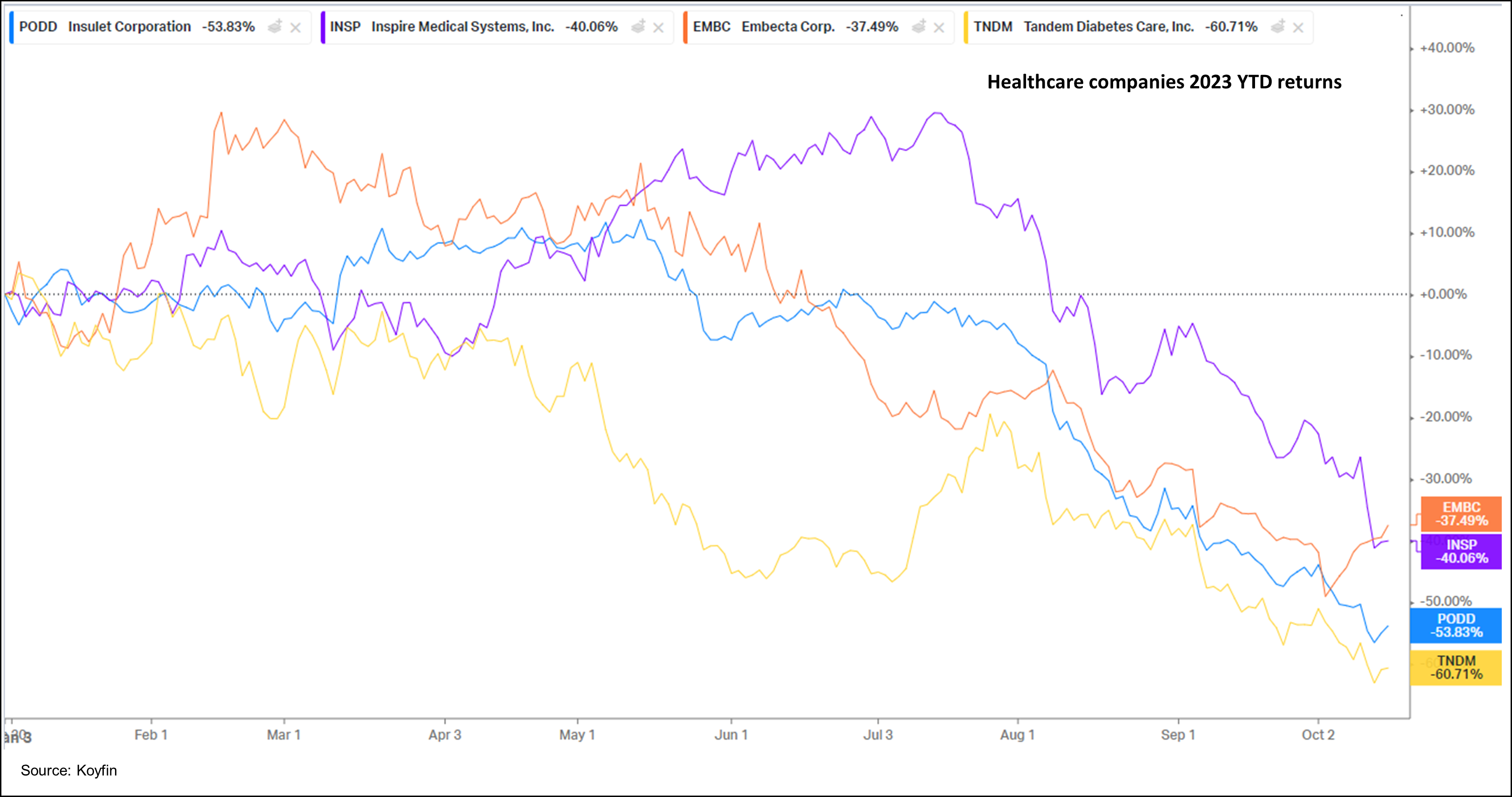

But outside the GLP-1 winners, such drugs have cast a long shadow over the future of several companies that in the past were perceived beneficiaries of the obesity of millions of people on the planet. We are paying heed to the stock prices of insulin pump-makers Insulet (PODD) down 48%, Tandem Diabetes Care (TNDM) down 64%, Dexcom (DXCM) a glucose monitor leader down 33%, all on ytd basis. Even businesses whose connection with obesity is tenuous at best, like those that produce C-PAP machines for people suffering from sleep apnea such as ResMed and Inspire Medical Systems, have seen their stocks being marked down 33% and 40% respectively this year. They were not alone to suffer the bloodbath of investors fleeing these stocks. Surgical robot maker Intuitive Surgical confessed that it had begun to see people deferring surgical procedures since they have heard about the arrival of the GLP-1s. While this is a small share of its overall business, it forms a growth segment nonetheless which has now come under a question mark.

Right now, investors are having none of any company seen to be at the receiving end of the anti-obesity narrative that is playing out loudly across Wall Street and America. The challenges of making GLP-1s available at the right price to the right patients at the right time are aplenty and a subject of an entire new piece. All the different elements of the healthcare system that require to pay up for these drugs (Novo’s Wegovy costs ~$16,000 per year) are not going to take it lying down and bear huge losses. Market estimates of the size of the anti-obesity drug market bandied around are wide, ranging from $30-80bn, with wild assumptions of demand and offtake being made right now. If proven true, that is the potential load they will place on the system which spent $421bn on outpatient drugs alone in 2021.

Even though one can argue that the price of these drugs will decline over time as new players come into the market, that will still take some years as they are still under clinical trials. Investors are not willing to listen to any reason just yet. Stock prices which have been hammered earlier this year remain depressed even today.

This is where the contrarian thinkers ought to step in. Some, if not all, could well be providing once-in-a-decade buying opportunities for long term investors who can take the current tumult in their stride. It is a time to go back, reassess and build conviction in a part of the market that skittish investors have thrown away and given up for dead right now.

Conclusion

We are not complacent about the potential structural changes AI can bring about in the world over time or the fact that anti-obesity pills could indeed prove to be the best thing to happen for laterally-challenged individuals. But we are equally convinced that the stocks that have been sold off in the melee for AI and GLP-1 pill stocks, present a clear opportunity to re-examine, ponder and reassess what the future might look like and whether the pessimism is justified once the hoopla subsides.

It is often said that the biggest upsides in investing come when the gap between perception and reality is at its widest. History is replete with instances of such extreme market behaviour towards either single stocks or sectors that, when proven otherwise, have driven the strongest period of stock returns as investors realize their folly.

Cover photo by julien Tromeur on Unsplash

End

Disclaimer

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Information has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. Opinions and estimates constitute our judgement as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This information is directed at accredited investors and institutional investors only.