Another month passes and it is another month of China stocks bashing done. We are referring to the mauling stocks have received in May when the Hang Seng Index dropped 9.1% with no real big reason to explain this. In this carnage lies a heap of good-to-great businesses, mostly treated shabbily by investors who right now do not wish to buy anything listed in Hong Kong, no matter whether or not the business involves China. As we see it, there are many companies that stand out, but there is one we are going to write about that merits attention, not just because it is makes for good value, but also because it happens to be a unique business in many ways which has few large peers that are listed. In Asia, it is by far and away the only such company we may have to invest in, in that space. We are talking about BOC Aviation (BOCA).

To the uninitiated, BOC Aviation is among the top five aircraft operating leasing companies in the world and the largest headquartered in Asia. It is owned 70% by Bank of China (BOC) and enjoys an A- investment grade rating from S&P and Fitch rating agencies. Its primary source of revenue is long-term USD-denominated leases contracted with a globally diversified portfolio of airline customers. It has a track record of over thirty years, having delivered a total of 822 aircraft and sold more than 400 and currently sits on US$22.1bn of assets.

Aircraft lessors stand between airframe manufacturers (like Boeing and Airbus) and airlines that wish to either own aircraft fully or partially or lease them through companies like BOCA. These companies are good proxies for air travel demand and growth of the airline industry over the long term. BOCA operates out of its head office in Singapore, where it has 162 of its 194 global employees. This is a small compact team of professionals that has honed special skills in buying and selling aircraft, leasing them to airlines, obtaining the best terms from manufacturers and raising money from diverse sources in financial markets at the finest possible rates.

Lessors like BOCA are often looked upon as sources of liquidity for airlines, especially in times of tight liquidity or flying conditions, and where airlines often seek to offload assets through sale-and-leaseback transactions. Banks are often found to be chary of, or simply lack the expertise for, executing such a complex financial transaction speedily. It is at such times (for instance recently during the pandemic) that BOCA steps in and conducts several such transactions, snapping up marquee airline customers like Singapore Airlines and Cathay Pacific in the process.

We explain this to impress upon readers the special skills required to conduct and operate this business with an industry counterpart that has traditionally been subject to high volatility and mortality. For a company to have built as solid a track record of financing aircraft over three decades and yet managed operating ratios that BOCA does today, is indeed worthy of mention. It is also why investors should be alert to an investment opportunity in BOCA shares such as we have today; it is a chance to buy a truly solid business that is built to last, and which has just recently come through its toughest trial by fire, the pandemic.

BOCA’s business was literally grounded through the pandemic when very few aircraft took to the skies and airlines were grounded with aircraft parked at airports and even distant deserted airfields in faraway lands. Many airlines simply bled to death or had near-death encounters until they were rescued by governments and, in some cases, by aircraft lessors like BOCA.

Through this utter chaos, BOCA surely took a few body blows as well, having to fend off airline delinquencies and delayed payments, having to repossess and redeploy aircraft at a time when nobody wanted them and having to refinance existing debt. This has to go down as the severest of real-life stress tests that any business could have modelled in their boardrooms and prepared for, and BOCA came through with no more than a few bruises. While the pandemic was the biggest stress test in its history, it has had other smaller yet powerful blows dealt to its balance sheet, also through events it could not have foreseen.

Most recently, the Russian-Ukraine conflict erupted, shutting out its six aircraft leased out to Russian carriers. That was a bolt from the blue and, despite its best efforts, BOCA might still have to kiss those aircraft goodbye as Russia has simply appropriated all commercial aircraft leased to Russian airlines. It is hoped that that is the final and last blow that BOCA has had to fend off. What this cemented was the resilience of the leasing model, evidenced further by the ability of the sector to absorb the $7bn of publicized impairments that resulted from the Russian invasion and the subsequent loss of over 500 aircraft.

The Skies Are Clearing

As we glide through 2023, we find that the stars are aligning for aircraft leasing again. Several factors are beginning to emerge that will put lessors with strong balance sheets and low funding costs at a distinct advantage in the years ahead. This comes at a time when the demand-supply equation for new aircraft is structurally turning favorable. Airlines now realize the need to rebuild old fleets, meet ESG requirements and build for growth and stay competitive in the future. The relevance of aircraft lessors could not have been more pronounced at any other time in aviation history.

BOCA has made a strong start to 2023. Aircraft and airline utilization rates and collection rates are improving. All aircraft scheduled for delivery in 2023 have been placed with airlines. It has raised US$1 billion in bond offerings from debt capital markets. BOCA possesses high liquidity of more than US$5 billion to fund debt obligations and anticipated capex, putting it in a good place to execute on its growth plans.

The Future Of Aircraft Leasing And Growth Outlook For The Industry Look Strong Again

Operating outlook for airlines is strong: The outlook for airlines and travel post-pandemic has been very strong generally. China too has come back, although its international connections are still limping slowly back to normalcy. This bodes well for aircraft leasing.

Travel demand to grow strongly: Even though much of the pent-up travel demand is now expended, travel demand continues to prove strong and resilient if forward bookings are any indication. Combined with China’s reopening, this has fueled a resurgence in air passenger capacity which had gone back to 100% of pre-pandemic levels by May 2023 as per a report by DBS Bank. Additionally, current high jet fuel prices vis-a-vis pre-pandemic levels and a growing emphasis on ESG compliance among airlines are stimulating demand for fuel-efficient, next-generation aircraft, thus driving aircraft replacement.

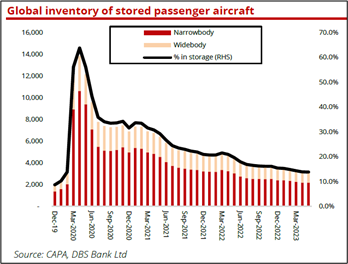

Aircraft supply-demand is tight: Aircraft supply may be tighter than it seems, as a large portion of the fleet of old, less fuel-efficient aircraft that were grounded during the pandemic, may never take to the skies again. Reluctant to scrap jets when prices for used parts and engines were low amid weak travel demand, airlines chose to keep the unwanted planes in storage. As a result, a significant proportion of the grounded fleet may have already been permanently removed from service, since it might not be economically feasible to return them into service.

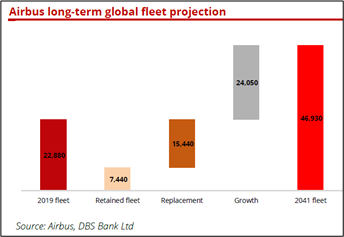

Aircraft replacement will be an important long-term theme for lessors like BOCA: Boeing and Airbus both project a doubling of the global aircraft fleet by 2040 from 22,880 aircraft in end-2019. Substituting older generation aircraft with new technology aircraft is now becoming an imperative for obvious financial reasons and also the desire and need by airlines to cut their carbon footprint. Approximately 40% of aircraft deliveries between 2022 and 2041 will be designated to replace older aircraft. As of Apr-23, there were around 4,183 passenger aircraft older than 20 years, constituting 16% of the global passenger fleet, that are immediately eligible for retirement. This potential phase-out could greatly reduce capacity in regions like North America, Europe, and the Middle East.

Protracted aircraft deliveries: Boeing and Airbus have never really managed to get ahead of their long-term production challenges, while the same can also be said of some of the engine manufacturers. This will potentially intensify an already prevalent shortage of aircraft. Between 2010 and 2019, global air passenger capacity expanded at a rate 1.6 times greater than global GDP growth. Nonetheless, by end-2022, the number of in-service aircraft was still 2% lower than in 2019, even though global GDP had risen by 6.8% over the same period.

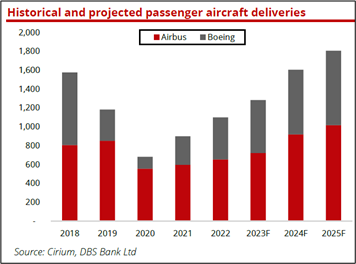

Airbus only delivered 181 jetliners in the first four months of 2023, a 5% decline yoy. While Boeing increased deliveries to 156 aircraft (+20.0% y-o-y), it warned that its delivery rate of the B737-MAX will drop due to certain quality issues it is facing. On the engine front, things are even more acute. New technology engines are proving to be less reliable than anticipated and are not staying on-wing as long as their predecessors did. Engine OEMs are compelled to divert new engines away from Airbus and Boeing and redirect them to airlines and MROs to ensure the existing fleet can keep flying. Consequently, aircraft deliveries may fall short of expectations again this year, and could remain below pre-crisis benchmarks (2018 as the base-year) until 2025, based on estimates by Cirium.

The operating share of lessors’ market is increasing: Since the inception of aircraft lessors almost fifty years ago, the trend line for operating lease market share has only gone in one direction. Over the course of the pandemic, the support lessors provided and the pivotal role they played in survival of many airlines have deepened and strengthened relationships between lessors and airlines.

With a greater appreciation for the flexibility that leasing offers and with several airline balance sheets still on the mend, lessors’ role has taken on greater importance in funding new deliveries. The percentage of leased aircraft has broken the 50% threshold, and it is likely that lessors are funding closer to 60% of new deliveries currently, either via their own order books or via the sale-and-leaseback channel. The dominant view from industry leaders is that, over the medium term, the overall percentage of leased aircraft is more likely to move towards the 60% mark than recede.

Further M&A and consolidation: The importance of scale has been a recurring theme and there is consensus that the importance of scale, from a leasing context, is likely increasing. As the leasing product becomes more commoditized, as lessors seek to chase the most attractive metal, scale will continue to be a differentiator. Those that can access the widest pool of debt and equity investors, that can control maintenance costs, that can maximize their purchasing power, are the ones that will be able underwrite larger transactions and grow faster.

This scale point has driven some material M&A over the course of 2021-22, with the GECAS-Aercap merger being the biggest and SMBC buying Goshawk more recently being another headline grabber. There is a belief that more consolidation is likely to take place in the near term.

BOCA Is Well-Placed

BOCA has several things going for it and one could argue that those advantages have improved and strengthened its relative position in the industry versus its peers.

- Low financing costs for BOCA – a key business moat

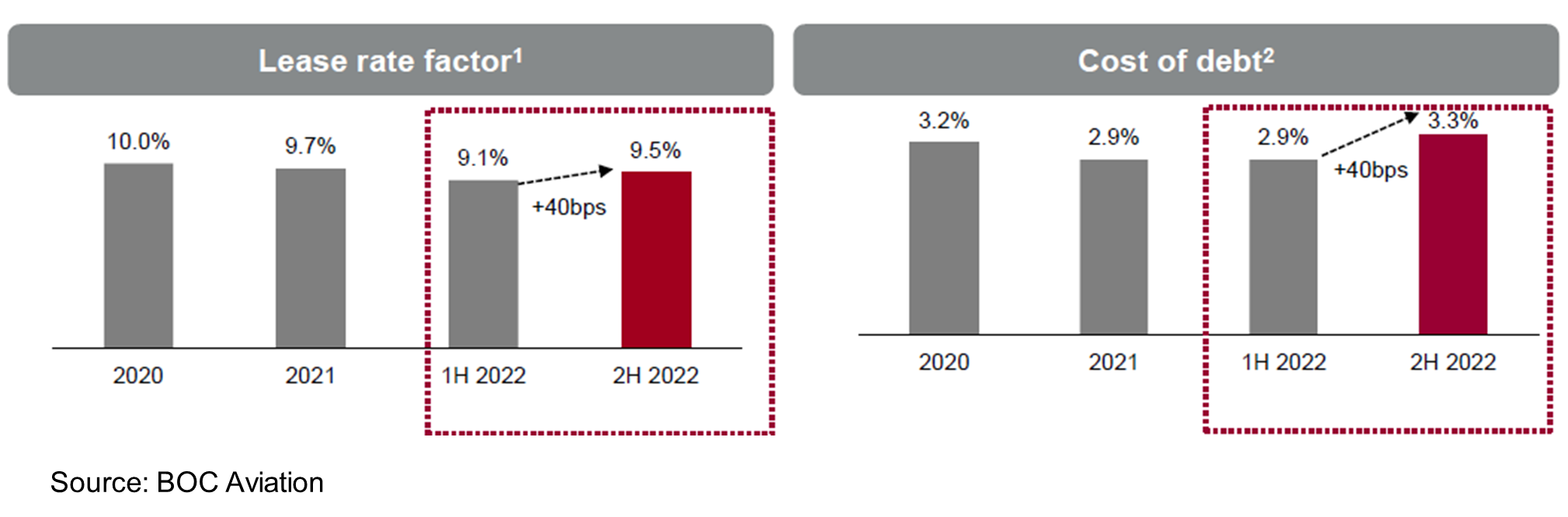

Even historically, BOCA has commanded the tightest spreads and best rates for borrowing from the market. Post the pandemic, its advantage could be said to have increased even further because of a few things that have transpired since. The table alongside shows the importance of low funding costs as a key competitive edge and moat for BOCA.

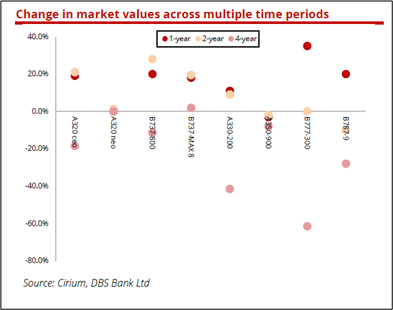

- Aircraft values are up across the board

Market values for new-build narrow-body aircraft are now higher than they were pre-pandemic. At the same time, market lease rates have also experienced significant growth in the past one year. Even middle-aged aircraft that lost value during the pandemic have seen notable increases. Market lease rates for wide–bodied aircraft are now at 95-100% of pre-pandemic levels.

We should expect lease rates for younger and mid-life aircraft to continue climbing, with more upside lying ahead. Recent statements from leading aircraft lessors have reported an acceleration in lease extensions and increase in aircraft sales to airlines.

One key point to note is that, given the lag between rising interest rates and lease rates, in the short term net lease yields could be pressured for lessors due to the rapid pace of interest rate hikes and aircraft delivery delays. Current robust lease rates are expected to have a more meaningful impact on portfolio yields from 2024 onwards, given the time gap between aircraft placements and deliveries, and Boeing and Airbus’ production rates begin to ramp up.

- Solid asset growth ahead:

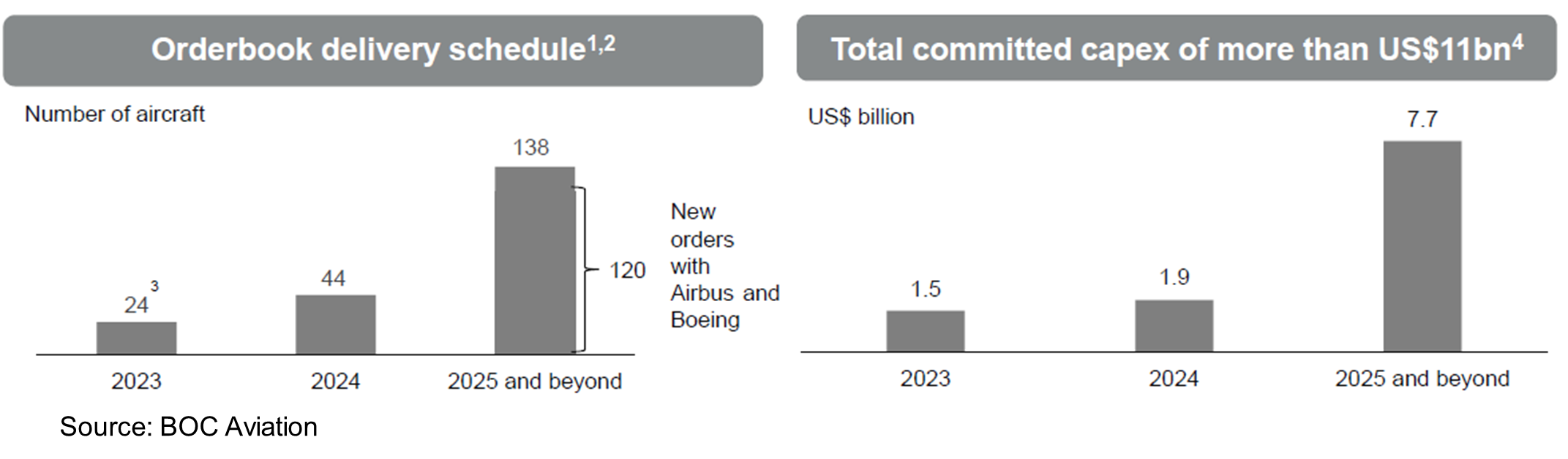

BOCA’s delivery schedule of aircraft and committed capex demonstrate high visibility of future growth. Two large orders with Airbus and Boeing have resulted in a total order book of 206 aircraft, providing a committed lease revenue of $16.8bn.

- Minimized impact of interest rate changes:

BOCA has low mismatch between fixed rate leases, which are a large proportion of its net book value, and the amount of fixed rate debt, which is high. Its debt maturity profile also shows that there is no large refinancing risk in any one given year in the future. BOCA’s investment grade rating and diverse funding channels in any case give it a distinct advantage to raise money at fine rates when required.

- Cash collections and operating cash flows are back up and strong again

BOCA’s collection rate hit 101% at the end of CY22 and it generated the highest operating cash flows at $2bn in CY22.

The Investment Case for BOCA

It is important to understand BOCA’s revenues and profit drivers and the value it has consistently derived from these over its history and would continue to do so in future.

Astute portfolio and active management of its fleet:

Its young fleet of narrow-bodied aircraft (4.6 years) places it in the right demand sweet spot of global aviation. Likewise for its ownership of new generation engines. BOCA has a well-honed strategy of selling aircraft and engines once they cross a certain age and where it strategically books gains on these at regular intervals so as to keep its fleet ‘fresh’ and current and in keeping with industry demands. This has been a significant value-driver and provides diversification from pure leasing revenues (see pie chart alongside).

Valuations and Distributions:

BOCA’s dividend policy of paying out up to 35% of PAT provides it with a good balance to fund growth and reward shareholders.

The BOCA stock has faced some turbulent times through the pandemic years, as one would have expected. Now, coming out of it, BOCA’s balance sheet is in a strong position and it looks set to embark on another growth cycle. The debate on ‘peak interest rates’ in the developed world is arguably a key headwind for the stock in the medium term. However, we believe that this is a good window of opportunity to get exposure to a high-quality business that has come through the severest test in its history with a relatively stronger position now.

The market uses P/B as the primary valuation metric to value aircraft leasing companies to reflect the capital-intensive nature of the business. BOCA’s P/B multiple before the pandemic averaged 1.1x while its P/E averaged 8x and dividend yield ~4.5%. Against that, BOCA trades at a P/B of 0.85x, P/E of 7.5 and dividend yield of ~5% on a 12m-forward basis. Importantly, its RoE trajectory ought to begin to rise over the next three years, getting to a level of 13-14%. The stock’s valuation ought to rise in step over this period.

Assuming the book value to grow to HK$80 by CY25 from its current HK$59, and applying a P/B of 1.2x we get a price range of ~HK$96, which is 60% higher in capital terms. Add in dividends and the total returns could rise to ~70% in this period. Not spectacular, but strong nonetheless.

Clearly, BOCA has emerged from the clouds of the pandemic and is now back to growing into a new aviation cycle.

Cover image by DCStudio on Freepik

End

Disclaimer

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Information has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. Opinions and estimates constitute our judgement as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This information is directed at accredited investors and institutional investors only.