It is well understood that the total returns an investor can earn from buying or owning a stock, over the period of his/ her holding it, is the sum of the capital appreciation on its price and the dividends she/he receives from the company. Simply put, Total Returns = Capital Appreciation or Returns + Dividends.

A vast majority of investors tend to focus most of their time and energy on the Capital Appreciation portion of this equation, while overlooking Dividends. They assume dividends to be an adjunct, an icing on the cake for their efforts, and sometimes dismiss and not factor in returns from dividends. We have even encountered sell-side research reports that provide copiously detailed financial analyses but miss out stating or forecasting dividends completely. We have also observed that in some countries where stocks tend to routinely trade at high valuations, the dividend yield on them is piffling enough for investors to not even care to know what dividends the company pays or has paid. Case in point: India.

Over the last few years, however, we have been struck by the number of companies in Asia that have been distributing copious amounts of the cash they have generated as dividends. Dividends have emanated not just from regular profits earned, but there have also been special dividends that some companies have paid out from their plentiful cash reserves. In some instances, the dividends surge is an outcome of the super-normal profits earned by these companies over a few years from commodity price inflation. However, if one were to go back in history to normal periods of commodity price fluctuations, the dividend yields even back then were well above market averages in such companies, suggesting an ethos and desire by such managements to pay out cash rightfully due to shareholders and not horde it. Investors would have done pretty well simply playing these cycles and exiting once the cycle appeared to have peaked. Thermal coal has been a great example of this in the recent past. More on this later.

We have never looked at or been attracted to the dividend yield of a stock in isolation. We have been aware that several companies tend to have weak or uncertain outlooks and weak balance sheets which puts the stability of the dividend itself in jeopardy and could eventually result in capital losses which far outweigh the dividends. We have also been wary of dividend yield stock screens put out by many researchers as the way to go in our hunt for yield.

Our quest for dividends has been both intentional and opportunistic. We have followed companies that have generated high free cash flows and where the propensity to pay out such cash flows is equally high, as the dividend policies are in place or aligned to the majority and minority shareholders. To get a better perspective and understanding of the nature of these dividend streams, we figured that we needed to think about these companies by slotting them in certain categories, which we elaborate below.

This helps us to:

- develop the right perspective on why we own a company or would like to own it;

- evaluate its fundamentals thoroughly to determine if those dividends are well-covered and sustainable through core earnings and not through any financial skulduggery; and

- if there are good reasons that the earnings will grow (slow but reliable is fine) which will lead to those dividends growing in the future as well.

Our focus and discussion in this newsletter are restricted to companies across Asia. We find that there is a general convergence of the sectors that tend to throw up such companies. These companies proliferate mostly within financials, commodities and materials, conglomerates/holding companies, utilities and some idiosyncratic sectors or situations and the odd consumer staple or discretionary sectors. We also find that state-owned companies in Asia are generous dividend payers.

We thus characterise these companies as:

- Type 1: Regular dividend payers/growers: These are companies which have stated dividend distribution policies and which deliver on that steadfastly. These companies simply generate sufficiently high free cash flows and have enough to spare after meeting their requirements to fund future growth (capex), working capital needs and repaying debt over time. These are typically the blue-chippy steady-eddies which run a fairly well-optimised capital structure.

- Type 2: Companies benefitting from super-normal profits in a cycle: These are companies which have run into a purple patch of profits, thanks to the cyclical nature of their businesses. Such a ‘purple patch’ might run from a few quarters to even a few years, giving investors enough time to partake in the riches being spewed out by such companies. There is a risk, though, that the cyclical downturn may arrive sooner than later and the quantum of dividends would decline with that.

- Type 3: Regular + Special Dividend Payers: Some companies have made it a policy to package their dividends as a combination of regular dividends (earned from profits for that year) plus special dividends added on and modulated so as to achieve a targeted dividend yield or absolute pay-out.

- Type 4: Holding companies: Situations exist where the holding company of the operating company needs cash (to service debts, usually), which expects or mandates the operating company to ‘upload’ as much of the profits it can to it. In this process, minority shareholders stand to benefit equally at the same time. It pays to own either the operating company or the holding company or even both, if they are listed.

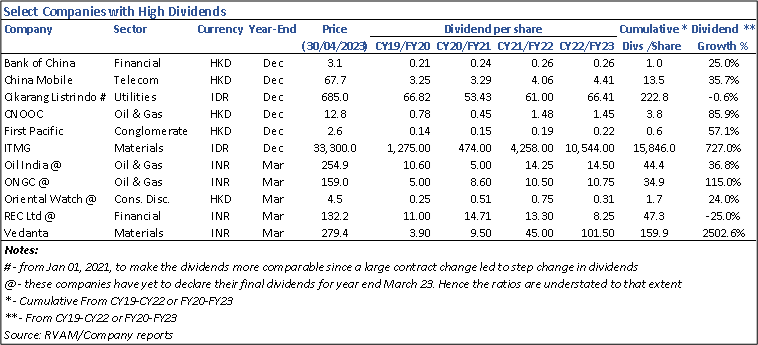

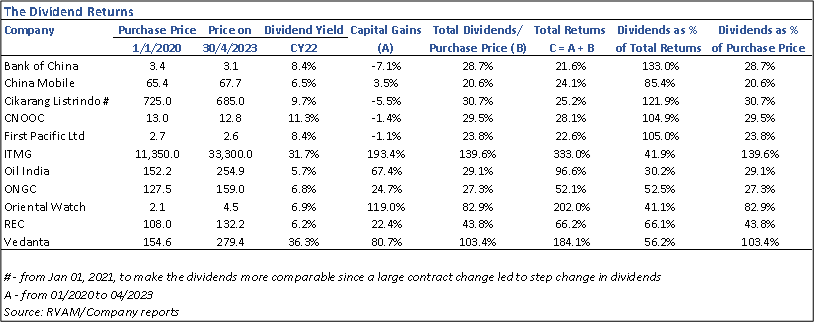

We have created a table of companies that we are familiar with and that we have followed for a period of time. This is not to be construed as a list of stocks we advocate anyone to buy, but can be used as an instructive way to appreciate the power of dividends in total returns.

We have assumed that these stocks were purchased on January 1, 2020, just before the pandemic hit. This list has provided us with keen insights on how some companies have navigated such environments and come out on the other side with their profits and dividends not just intact but even having grown.

Below, we elaborate on some examples and slot them in those boxes we have created.

Bank of China (BOC), China Mobile and Rural Electrification Corporation (REC) are the typical Type 1 companies. BOC and REC are financials, while China Mobile is the largest telecom operator in China. All three have delivered unspectacular but steady growth through the pandemic years. Coming out of it, dividends have in fact been stepped up strongly at China Mobile and REC. In all three cases, dividends have been a larger part of their total returns than capital appreciation by a significant margin.

The ones that were the true dividend gushers have been the Type 2 variety. Here, Vedanta and ITMG stand out. Vedanta Ltd (VDL) is a peculiar corporate situation where the holding company, Vedanta Resources Ltd (VRL), is where the group debt resides and needs to be serviced through dividends to be uploaded by Vedanta Ltd. Since VRL has a bunch of debt repayments/ refinancing obligations falling due between 2023-2025, VRL needs to keep its eye on every dollar it can get its hands on from VDL. This has benefitted minority shareholders hugely over the last two years.

Anybody who had the foresight to visualise the situation in early 2020 could have made out like a bandit since. Vedanta Ltd has paid dividends cumulatively worth Rs. 160 per share since January 2020 against a stock price of ~ Rs.155 back then. A whopping 100%! Today, the current market price of the stock is ~Rs.275. The tough part of this bet in 2020 was the need to take a view on the price of crude oil, zinc and aluminium, three years out, just when the world was entering the ghastliest phase of the pandemic and an exit from it looked opaque at worst. Even a purchase of VDL made less than two years ago, in say January 2022, when the price was around Rs. 340, would have yielded gross dividends of Rs.114 since.

The learning from such a situation is that it often pays to analyse corporate actions at companies like these closer than we usually do, above and beyond the fundamentals of the operating company. Corporate exigencies, like those at VRL alone, become the bulwark of the buy-case here as, without dividend support from VDL, VRL would be in a dire state of default, an eventuality that the owner can ill-afford. It is now apparent that Vedanta will continue to pay out all the dividend it possibly can for at least another two years as the holdco VRL has large refinancing/ repayments due in this period.

In the case of ITMG, a coal miner in Indonesia, it was simply manna from the gods in the form of thermal coal prices. Prices of thermal coal rose from the mid-2020 trough of $55/t to reach an astronomical high of $430/t by September 2022, a near eight-fold increase! Coal miners like ITMG have made more money in the last two years than they ever have in their history.

The reason we picked ITMG as a case study is that its parent, Banpu Coal, listed in Bangkok, needs the cash flows from its coal mining operations in Indonesia to finance its power utility growth ambitions in Asia. To achieve its growth capex and sustain debt covenants, it has held fast to a dividend pay-out policy at ITMG of a minimum of 70%. ITMG has often exceeded this in the past when its own cash requirements have been low. The riches from the thermal coal profits of the past two years have proved to be the proverbial gusher investors can only fantasize about. Anyone who bought ITMG in early 2020 has been repaid the cost of his purchase and more through dividends alone since then. The stock traded at between IDR 10,000-11,000 then, while it trades at ~IDR 27,000 per share today! Clearly, the forward outlook for thermal coal is now weaker and prices have come off sharply, suggesting that dividends too will decline in step in the future.

The most difficult ones to unearth are the Type 3 variety of companies. These tend to be the under-the-radar small/mid-cap stocks that keep cranking out solid numbers year after year and keep their loyal flock of shareholders happy by paying out not just regular and growing dividends but also generous dollops of special dividends along the way. Hong Kong Stock Exchange has plenty of listed companies which follow this path. One such name we have known for a long time is Oriental Watch Ltd (OWL), a watch retailer owning shops in HK/Macau and Mainland China. OWL is a small cap company that would not figure in the scheme of things at any large institutional investor. Yet, it is in this area of the market where such gems are to be found.

Oriental Watch held HK$1.1bn in cash and equivalents at the end of CY19. The stock traded between HK$ 1.9 – 2.0 per share in January 2020. Between then and today, OWL has paid out HK$1.70 per share cumulatively as dividends (regular + specials). OWL has yet to declare its final dividend for the year ended March 2023. So OWL’s aggregate pay-out numbers will look even more incredible in a few months from now. OWL’s business has weathered the pandemic storm like few other consumer discretionary companies we know have. Now that HK/Macau and China are back to business as usual, OWL’s watch retail sales ought to continue to grow. Note that nearly 90% of OWL’s watch sales comprise sales of Rolex watches. OWL is a classic “gift that keeps on giving”.

Finally, we come to Type 4 which are the holding companies. Once again, HK abounds with old school traditional family-owned conglomerates built on the edifices of property development and ownership of offices, retail malls, infrastructure assets, etc. However, several of them have fallen from grace and popularity with investors owing to various reasons that are not in the ambit of this discussion, hence we shall not delve on these reasons here. However, there is one facet that these conglomerates possess that keeps a certain body of investors still interested in them, especially after the sharp decline in their stock prices over the last three years. We have picked one of the smaller ones listed in HK, First Pacific Company Limited, for discussion here.

First Pacific is a Hong Kong-based investment holding company with investments located in Asia-Pacific, engaged in consumer food products, telecommunications, infrastructure and utilities and natural resources. It is owned by Mr Anthoni Salim, who is Indonesia’s premier businessman, and is one of the largest business groups there. First Pacific owns well-known listed companies such as Indofood Sukses Makmur (consumer staples), PLDT (telecom operator in Philippines), Metro Pacific Investments which holds investments in monopolistic water and power utilities and toll roads in the Philippines and a clutch of smaller natural resources businesses.

First Pacific receives its share of dividends from these operating companies each year. All the underlying companies are well-entrenched, profitable near-monopolies and mature businesses with healthy cash flows. These companies upload steady and large dividends to First Pacific each year. First Pacific in turn pays dividends to its shareholders from these dividends after providing for its corporate costs and servicing the debt it holds. First Pacific has committed that future acquisitions will happen at the operating company level if any, and not at the First Pacific holdco level as was the case historically. This will allow First Pacific to continue to step-up pay-outs even further in the future, as it has already demonstrated in the last two years.

First Pacific’s stock trades at half its book value of HK$6 today and at a discount of ~55% to its NAV as against a 20-year average discount of 45%. The dividend yield of over 10% which looks solid and sustainable is a huge incentive to own what appears to us as a bond-like proxy with modest equity upside should the market compress this prodigious dividend yield closer to its peers which trade at yields between 4-8% sometime in the future.

The attraction of looking at dividends in such a light has proved more insightful and rewarding. Along with the capital appreciation upside embedded, such stocks are better supported by these prodigious and stable dividends over longer periods of time. Of course, it must be admitted that over short periods market volatility can lead to short term capital losses, which investors need to ride out.

The term, “the gift that keeps on giving,” apparently originated, at least in the United States, in the mid-1920s as a slogan advertising the newly invented phonograph. The phonograph was a remarkably successful invention and one can see why the slogan would have been applied – once you have one, you can keep on listening to your favourite records. So the slogan, unlike most advertising slogans, was truly appropriate.

The “gift that keeps on giving” phrase became increasing used to continually invoke the feelings people get when they receive a gift. It implies that any present that gives enjoyment over and over again, such as a radio, camera or a magazine subscription, would be better than a gift that only provides that feeling once, like a bouquet of flowers. The phrase was especially popular with electronics companies and some of the most well-known commercials used the phrase.

It is amazing why we in the investment world do not view dividends and dividend paying companies in a more genteel light and with greater respect for the vast value we derive from them. Dividends just need a little more love and appreciation for being the gifts that – well – keep on giving!

(cover image photo by micheile henderson on Unsplash)

End

Disclaimer

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Information has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. Opinions and estimates constitute our judgement as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This information is directed at accredited investors and institutional investors only.