Our macro view incorporates certain trends that we project over the next few years. These trends form the bedrock on which the portfolio is constructed. To ensure that this macro view is on track we will continue to monitor certain macro variables on a regular basis. The underlying principle is that these are our well-considered long term views and hence should not require to be changed dramatically or frequently.

Our macro view consists of the following beliefs:

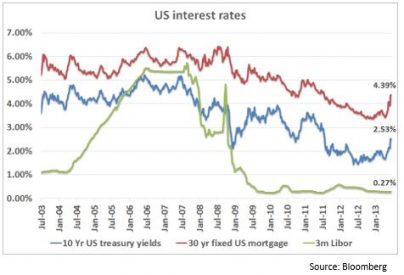

1. We are at the bottom of a long term interest rate cycle

This is (and has been) our strong view. The greyness is regarding the level and pace of interest rate increase going forward. Our projected base case is a slow and steady increase in the long term rates from now on and no movement in the short term rates for the next 18 months.

The chart on the right shows the long term trends in certain benchmark rates. Though the longer term benchmark rates have spiked up in the past month, they are still well below the peaks of even the last five years.

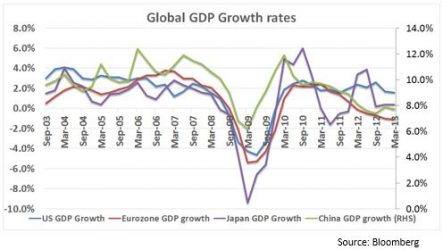

2. Growth is going to remain anaemic globally

Our view is that the financial leverage built up over the past three decades is slowly reducing. This deleveraging has a negative impact on potential growth. It is our view that this deleveraging will fortunately be a slow trend or else the impact would have been more catastrophic. This is especially true in the developed world.

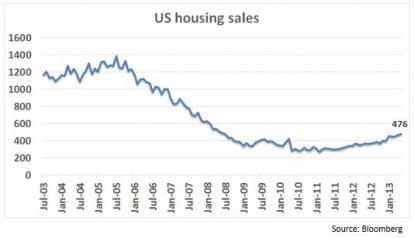

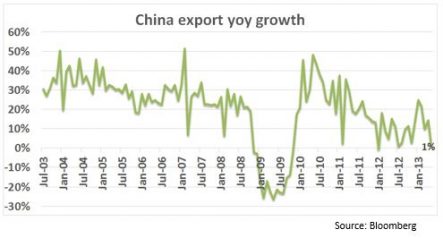

The chart on the right shows the slowing down of GDP growth in the four large economic blocs of the world. We also look at US housing sales as a surrogate of US economic growth (see chart below). Though this has rebounded off the bottom, it remains much below the peaks of 2006. Finally we look at Chinese export growth as a surrogate of global trade and this number is much below long term averages (see chart below right).

3. Slow directional change in equilibrium for both ‘growth’ and ‘interest rates’

We are at equilibrium now with a slow change in direction both for growth and interest rates. Both will move up, but slowly.

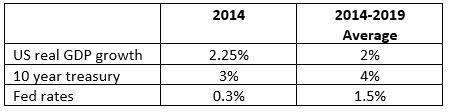

The recent spiking of mortgage rates in the US is going to have a downward pressure on the real estate sector and will pull down growth. This in turn would reduce the need for rates to go up. So there is a constant balancing act between interest rates and growth – and the current equilibrium is only going to move up gradually. The table below states our medium and long term macro expectations.

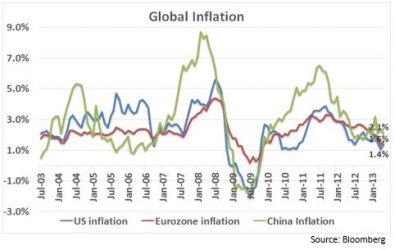

4. The real party spoiler could be inflation

If inflation starts to rise before growth comes in or before deleveraging is done, then the party will stop very abruptly. Fortunately, current inflation numbers across most parts of the world are below long term trend lines as shown in the chart on the right.

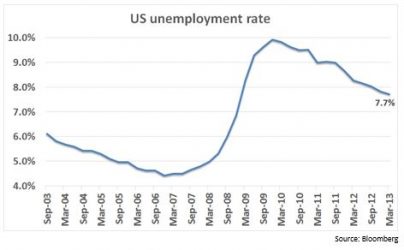

Inflation is not a concern in the short term as spare capacity in the form of unemployment rate remains high (refer chart below showing the US unemployment rate from 1993 to 2013).

This summarizes our macro view.

End

Disclaimer

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Information has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. Opinions and estimates constitute our judgement as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This information is directed at accredited investors and institutional investors only.