Executive Summary

The AI narrative and value creation have mostly been monopolised by the AI infrastructure build out, the LLM leaders’ investments (and valuations) and the agentic AI implementors across industries. The crucial question now is: Has the AI spend by bricks and mortar companies actually started having a beneficial impact on their financials? It might still be early days to get a clear answer but, without an empathic “Yes” in the next few years, the full AI story will collapse. To explore this question, we looked at the FMCG sector across the world, including food, personal care and household products. Specifically, we examined ten companies in this sector – Unilever, Procter & Gamble, L’Oréal, Nestlé, Coca-Cola, Reckitt, Colgate-Palmolive, Danone, Mondelez and Beiersdorf.

Across these ten global consumer companies, artificial intelligence has moved decisively out of the pilot phase and into core operations. Every company reviewed now runs AI in production across some combination of marketing, product development, and supply chain. The strategic question is no longer whether AI works in FMCG, but where it creates measurable value, and, critically, whether that value shows up as faster revenue growth or as lower cost and higher margin.

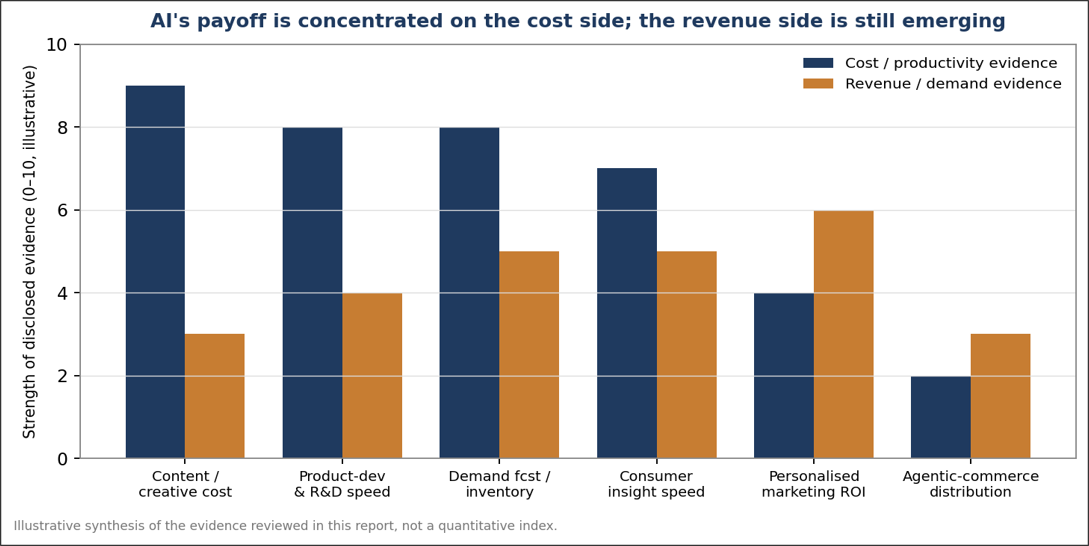

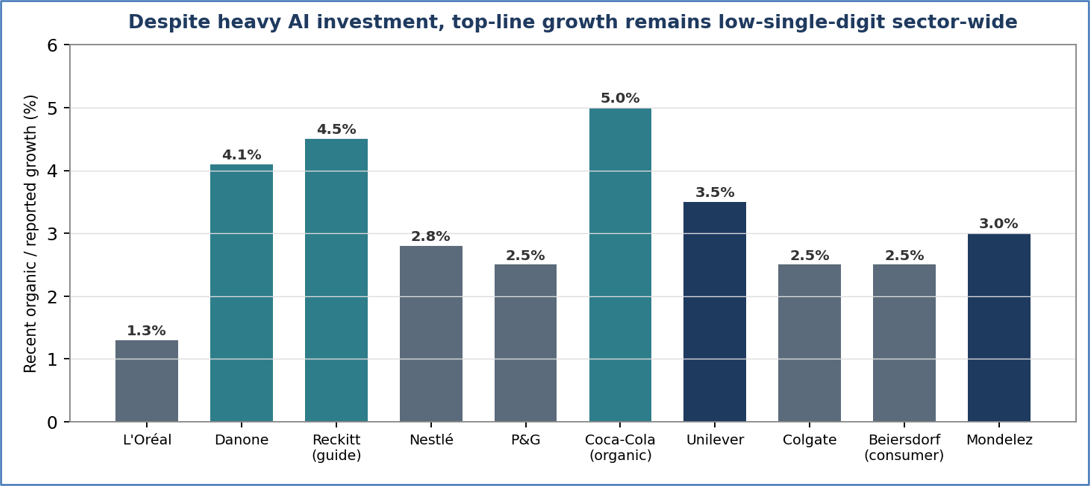

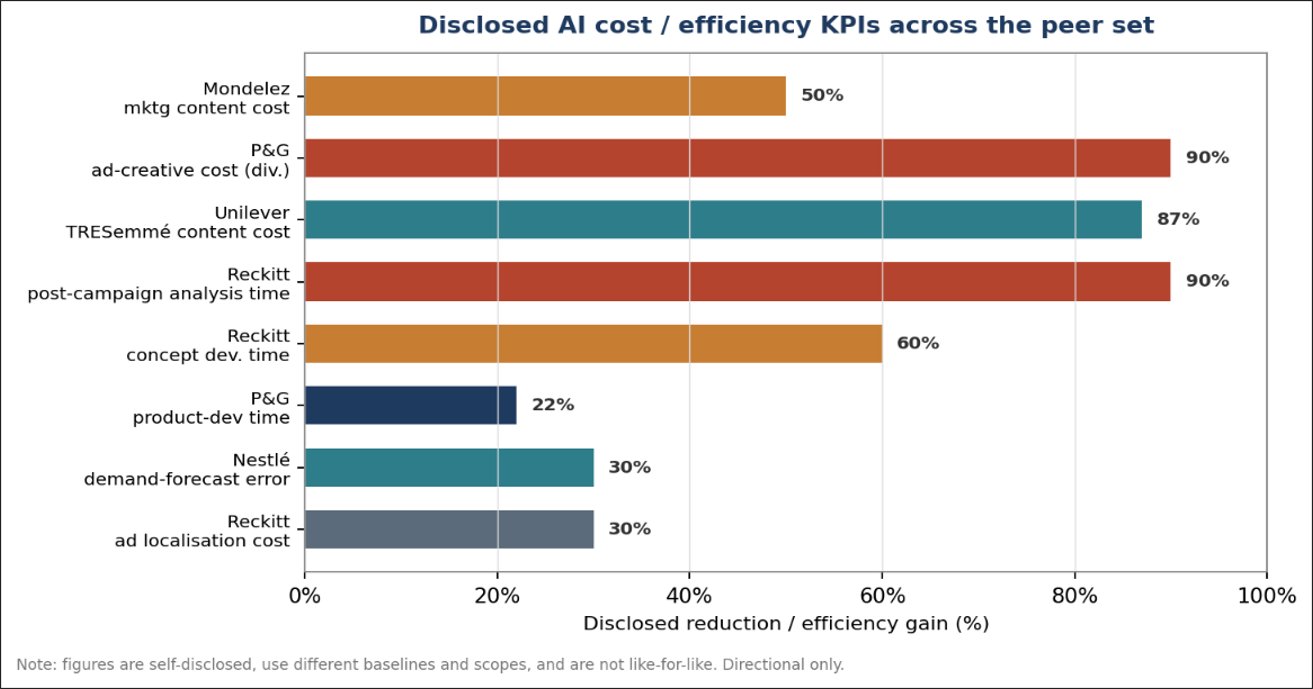

The evidence points overwhelmingly in one direction. The best-quantified, most repeatable payoff from AI so far is on cost reduction (in content production, product-development speed, demand forecasting, and consumer-insight generation), not on demand creation. Companies routinely disclose 30-90% reductions in specific cost or time lines, when AI was used e.g. Mondelez’s marketing content cost down 30-50%; a P&G division’s ad-creative cost down ~90%; Unilever’s TRESemmé Thailand content cost down 87%; Reckitt’s concept-development time down up to 60%. By contrast, direct AI-to-revenue attributions are rare, single-case, and modest, e.g. Unilever’s TRESemmé +5% purchase intent, Nestlé’s field-sales tool crediting +3% sales in major accounts. Sector-wide, top-line growth remains stubbornly low-single-digit despite the AI investment surge.

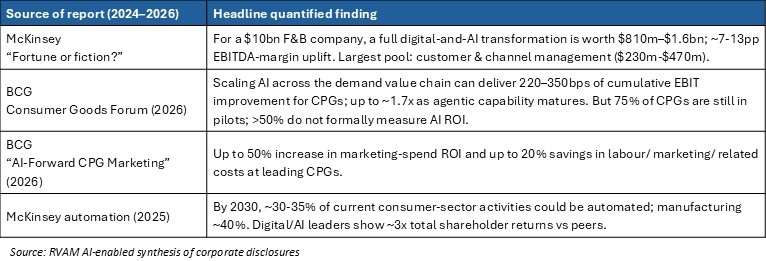

The macro framing supports this. McKinsey estimates that, for a $10 billion food-and-beverage company, a full digital-and-AI transformation will create value worth $810 million to $1.6 billion, which is driven by an EBITDA margin uplift of roughly 7-13 points, with the value split across both top line and productivity. BCG puts the cumulative EBIT prize at 220–350 basis points for consumer packaged goods (CPGs), while cautioning that much of it is likely reinvested into pricing and product rather than dropping to margin. Both houses agree that the near-term, bankable gains are efficiency gains.

Key Findings at a Glance

- No single “AI winner” AI is becoming a sector-wide efficiency reset. L’Oréal has the strongest combined case (deepest R&D-speed and consumer-engagement claims plus above-market growth), and P&G the most rigorously quantified cost numbers, but neither has translated AI into a durable growth breakout.

- Cost is proven; revenue is a bet. Marketing-content cost and product-development speed are where hard numbers cluster. Revenue upside hinges on personalised marketing at scale and on agentic commerce, both real but largely unproven at group level, and mostly a 2027+ story. See chart below.

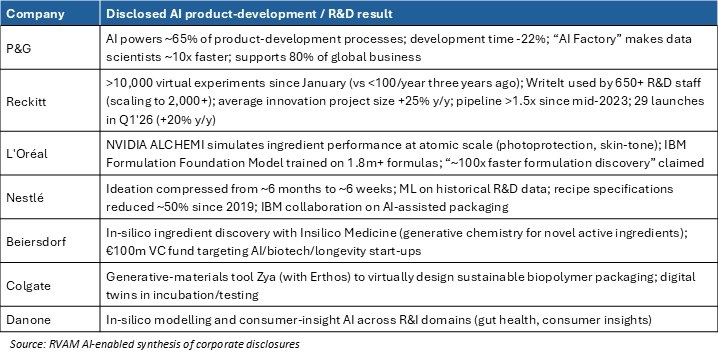

- R&D is the fast-emerging second front. L’Oréal (usage of NVIDIA ALCHEMI solutions and IBM’s AI-based formulation models), Reckitt (>10,000 virtual experiments since January vs <100/year three years ago), Beiersdorf (in-silico ingredient discovery) and Nestlé (ideation compressed from ~6 months to ~6 weeks) show AI compressing innovation cycles materially.

- Food & beverage leans supply chain; beauty leans R&D and personalisation. Nestlé and Danone concentrate on demand forecasting and revenue-growth management, L’Oréal and Beiersdorf on formulation and consumer diagnostics and the home-and-personal-care names on content production at scale.

- The competitive risk is parity, not disruption. Because everyone is deploying comparable tools, AI may preserve relative position rather than confer lasting advantage, with margin being the battleground.

Source: RVAM AI-enabled synthesis of corporate disclosures

The Two-Channel Framework

We examined the impact of AI across two headers for these ten consumer companies: (1) the impact on revenue growth and (2) the cost improvement they are extracting using AI in their business.

Revenue drivers: These include better understanding of customers (AI-synthesised consumer insight, search-signal mining, diagnostic tools), better positioning of new products (AI-guided concept generation and testing), personalised marketing at scale, and (the newest lever) being discoverable and recommended inside AI-mediated “agentic” commerce.

Cost savings: These include advertising and content-production cost (AI-enabled creatives, localisation, adaptation), product-development and R&D cost (in-silico formulation, virtual experiments, faster ideation), inventory and supply-chain cost (AI demand forecasting, promotion optimisation, logistics routing), and back-office/ enterprise productivity (copilots, agentic process automation).

Some potential sector-level benefits over the medium term

Some of the potential impact from these AI spends was elaborated in reports from McKinsey and BCG in the last one year. A few findings are elaborated below.

Revenue Drivers: Understanding Customers and Positioning Products

There are multiple ways in which each company is using AI to grow the top line: understanding customers more deeply, positioning and launching new products and, increasingly, engaging consumers directly through AI tools. The honest headline is that revenue-side evidence is thinner and more anecdotal than cost-side evidence, but it is growing. It is also most developed in the beauty industry.

Some typical examples of what these companies are doing will give us an idea of where this effort is headed under various sub-categories.

Understanding the customer

L’Oréal operates what it calls the world’s richest beauty dataset (seemingly ~14,500 terabytes) and its “Consumer Loop” platform capturing millions of real-time ratings across 150+ countries. Its consumer-facing Beauty Genius assistant generated over 1.1 million conversations in the US, and its L’Oréal-backed marketplace Noli is built on 1m+ skin data points. The stated shift is from “beauty for all” to “beauty for each,” with augmented reality (AR)/AI diagnostics explicitly credited with reducing product return rates.

Colgate-Palmolive mines global search-engine data with machine learning to cluster consumer questions about oral health into unmet needs, feeding them directly into early-stage product development and clinical strategy. It uses generative AI to “synthesise consumer insights” and give instant answers to local business questions drawn from its full internal history of insight reports across geographies and categories.

Nestlé processes insights from 340m+ first-party data records to fuel targeted campaigns and runs 45 content studios generating personalised digital content. Its “NesGPT” internal assistant supports insight and content work across functions.

Coca-Cola has re-framed its strategy around “persuasion-led” growth – using AI and digital platforms to shape demand rather than lean on price – and shifted digital from <30% of media spend (2019) to ~65% (2024).

Beiersdorf built the NIVEA SKiN GUiDE selfie-analysis web app on 12m+ skin images from 10,000 women, using it both as a consumer diagnostic and as a first-party data engine. Its work with Automated Creative tags every creative asset so that the company can understand “the DNA of a top performer” i.e. why an ad works, not just which one did.

Positioning and launching new products

Nestlé has compressed product ideation from roughly six months to six weeks using generative AI, and uses ML on historical R&D data to accelerate idea generation. Colgate tests products in an incubation phase using digital twins and virtual panels, then uses AI to generate thousands of market-customised content assets, a model it used to roll out whitening toothpaste globally after an initial China success.

Coca-Cola’s Y3000 Zero Sugar was co-created with AI by analysing large volumes of consumer discussion about the “taste of the future.”

Reckitt reports its “digital active learning” approach reduced the error rate in predicting consumer perception by 75% and lifted overall consumer liking from 8.4 to 9.1 on Vanish Turbo, thus showing a rare and concrete link between AI use and product-market fit.

Mondelez ran ~40 campaigns as controlled experiments before scaling, and reports personalised marketing delivering 20-30% higher ROI. This is the justification for its $40m generative-AI build.

The newest lever: agentic commerce and AI-mediated discovery

Several companies are explicitly positioning for a future where consumers discover and buy through AI assistants. Unilever’s five-year Google Cloud partnership (Feb 2026) is the clearest wager that being algorithmically “recommended” by AI shopping agents becomes a real distribution channel. L’Oréal’s Noli marketplace and Beauty Genius, Coca-Cola’s Azure OpenAI assistants, and Colgate’s LLM-driven digital-shelf tools all point the same way. This is a structural, multi-year bet: value would show up as volume growth with a lag, not necessarily in the next few quarters.

The broad conclusion is that the impact on AI effort on topline has a lot of promise but has shown minimal impact so far. Despite heavy AI investment, growth remains at low-single-digit-level almost everywhere, underscoring the fact that AI has not yet produced a demand breakout at any of these companies (see chart alongside).

Source: RVAM AI-enabled synthesis of corporate disclosures

Cost Savings: Advertising, Product Development and Inventory

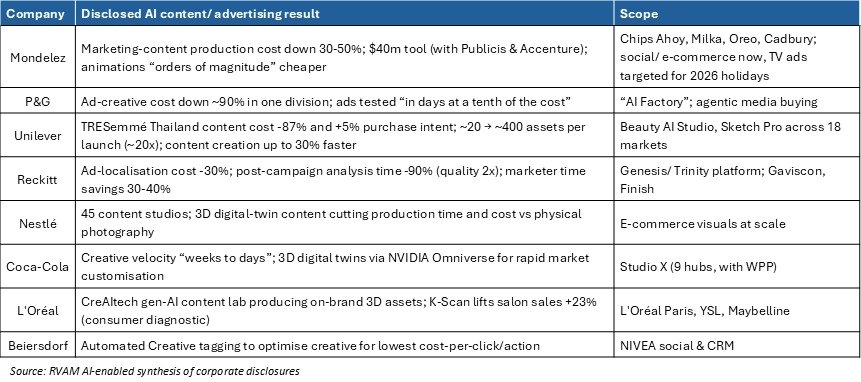

This is where the hard numbers are. The disclosed AI results across all ten companies cluster in three cost pools: content/ advertising, product development/ R&D, and inventory/ supply chain, overlaid by a fourth, enterprise productivity. Below, each pool is collated with the most-comparable quantified figures on record.

Advertising and content-production cost

Generative AI’s first and most mature FMCG use case is producing, adapting and localising marketing content. The figures are striking because content production has historically been a large, agency-heavy line item.

Product development and R&D cost

The second front – compressing the innovation cycle – is where beauty and health players are moving the fastest, using in-silico simulation to replace or front-run physical lab work.

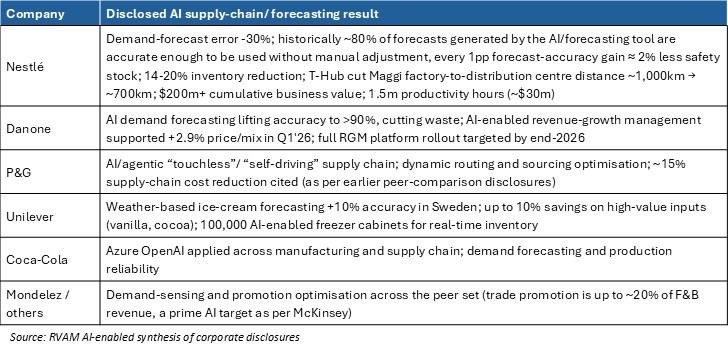

Inventory, demand forecasting and supply-chain cost

The food-and-beverage names lead here, because perishable inventory and complex logistics make forecasting error expensive. This is also the pool McKinsey and BCG both flag as having the clearest, most bankable ROI.

Enterprise productivity and back office

Beyond the three core pools, every company is deploying copilots and agents for general productivity. Danone rolled Microsoft 365 Copilot to 50,000+ employees and deployed autonomous agents in HR and order-to-cash, reducing manual errors, billing disputes and speeding order handling. Coca-Cola’s $1.1bn Microsoft commitment targets “time-to-answer” reduction across functions. Colgate’s AI Hub lets employees build and deploy their own assistants at scale. Nestlé uses AI to automate finance data-cleansing and forecasting and was selected for the Harvard D^3/ Microsoft Frontier Firm AI Initiative.

Source: RVAM AI-enabled synthesis of corporate disclosures

Where is the Value Landing?

Pull the evidence together and a clear pattern emerges. The proven, near-term value of AI in consumer goods is a cost-and-productivity story with three legs, content, R&D speed, and forecasting, reinforced by broad enterprise-productivity gains. The revenue story is real but still in the early days, is thinner, and concentrated in beauty and in revenue-growth management. This mirrors exactly what the Unilever deep-dive found at a single-company level, and it holds across all ten names.

Two structural facts explain the asymmetry. First, cost/efficiency gains are internally measurable and quickly bankable whereas demand creation is multi-causal and hard to attribute to AI versus other factors like pricing, portfolio, or category tailwinds. Second, the single largest revenue lever, agentic commerce, is a distribution bet whose payoff is inherently lagged and not yet visible in any of these companies’ numbers.

Sub-sector differences

- Beauty (L’Oréal, Beiersdorf; Unilever/Colgate personal care): R&D formulation + consumer diagnostics + personalisation. AI fits the structure best; the strongest revenue-adjacent claims are here.

- Food & beverage (Nestlé, Danone, Mondelez, Coca-Cola): demand forecasting, revenue-growth management and, for the beverage/ snack marketers, content production. Supply-chain ROI is the clearest bankable pool.

- Home & health/ hygiene (P&G, Reckitt, Colgate home care): productivity, content at scale, and virtual-experiment R&D, often tied to explicit cost-ratio targets.

Is anyone winning?

On the combination of quantified AI activity and actual top-line performance, L’Oréal has the strongest overall case (deepest R&D-speed and consumer-engagement claims, above-market growth). P&G has the most rigorous cost numbers. Nestlé owns the supply-chain lever. But no company has converted AI into a durable growth breakout. Every name here is still growing at low-single-digits. The most likely sector outcome is a shared efficiency reset that preserves relative competitive position with margin as the battleground. GlobalData’s own “AI leaders” list (Coca-Cola, PepsiCo, Unilever, P&G, L’Oréal, Estée Lauder, J&J) is itself evidence that AI is becoming a basic requirement rather than a differentiator.

Conclusion

The level of growth that global consumer companies are extracting from AI today is, based on disclosed evidence, primarily a margin-and-productivity story, not yet a revenue-growth story. Across all ten companies, the best-quantified results are cost, speed and efficiency metrics. Direct AI-to-revenue evidence exists but is scattered, single-case, and modest against low-single-digit group growth.

This matches the macro estimates: McKinsey’s $810m-$1.6bn prize for a $10bn F&B company and BCG’s 220-350bps of EBIT are real and large, but front-loaded on the cost side and, as per BCG, likely reinvested rather than banked as margin. The revenue breakout, if it comes, depends on two things that are largely unproven at group scale: personalised marketing replicating its single-campaign wins across whole portfolios, and agentic commerce becoming a genuine distribution channel. Both are 2027-and-beyond questions.

What to watch

- Whether demand-side wins (cost down AND purchase intent up) replicate across multiple brands and markets, not just showcase campaigns.

- Whether agentic-commerce positioning (Unilever/Google Cloud, L’Oréal Noli, Coca-Cola Azure) produces measurable share-of-recommendation or conversion data as AI shopping assistants scale.

- Whether any company sustains above-category growth that it can credibly attribute to AI rather than pricing, portfolio or category tailwinds, which would be the single strongest signal that the effect is real and scalable.

- Whether disclosed cost savings actually drop through to reported operating margin, or get competed away/ reinvested as BCG expects.

For an investor or analyst, the practical implication is to treat AI in FMCG as a margin and competitive-parity theme first, and a growth theme only on evidence, and to disentangle AI-driven improvement from the structural portfolio. The stock prices tend to reflect this AI-led evolution at almost every one of these companies.

Cover image by rawpixel.com on Magnific

End

Disclaimer

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Information has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. Opinions and estimates constitute our judgement as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This information is directed at accredited investors and institutional investors only.