Why look at the 5-year plans?

As another year comes to an end, it is a time to reflect. Our fund had its strongest year in absolute terms in 2025 (2024 was our best year before this year). This is on the back of a strong reset of asset prices in Asia and especially in China which is our core market. To better understand this, it is important to get a deeper insight into the movement in the long-term drivers of China at the macro level, industry level, regulation level and company level. Without this we will surely miss the wood for the trees and be simply driven by the broader deluge of noise that tries to drown out investors on a daily basis.

To obtain this insight, a good place to spend some time on is China’s 5-year plans. For most people these are anachronisms from China’s socialist past and something to ignore. We beg to differ. We believe they give insights on long term changes in the government’s focus areas. If we view Chinese policy movement as a large super tanker, these 5-year plans are the slow direction changes being steered by the captain – not perceptible in the short run but very clear on a larger time window.

Our attempt is to try and connect the last two plans (the 13th & the 14th) with the latest plan (the 15th) announced in late 2025, and highlight aspects that are losing or gaining emphasis, new focus areas that are coming up and old focus areas that have been dropped.

Firstly, the way this works is that the KPIs for party and government functionaries at all levels get aligned to these plans. As that happens, we see a gradual but sustained movement of public and private capital, tax breaks, regulatory tailwinds, new company creation, etc. towards these focus areas. This makes complete sense as the local leaderships’ upward promotion in the power structure are dependent on achieving these new KPIs. This process is certainly slow, but it is inexorable.

Secondly, the plans consistently focus on the bulk of these areas over a long period of time. This is the advantage of having a ruling structure that does not change every 4-5 years, though this also carries the risk of a slower course correction in case a wrong strategy has been emphasized. On balance, the chance of these strategies succeeding is higher since the local incentives have been aligned and the process is given a long enough time window to succeed.

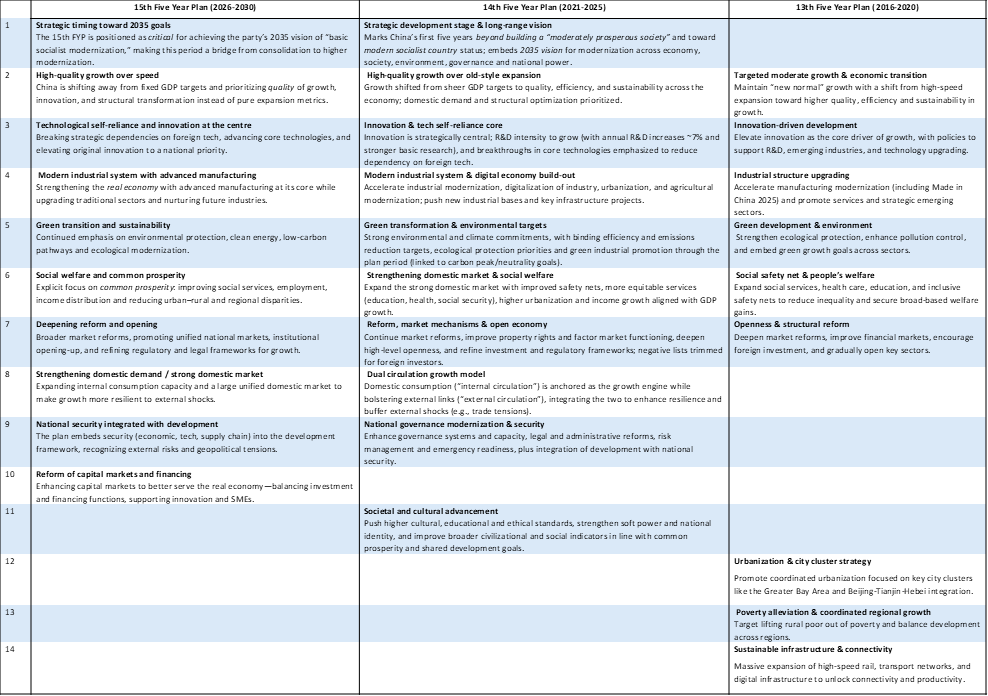

As a starting point, we asked ChatGPT to give us the ten most salient focus areas of each of the last three 5-years plans. We used its basic output to compile the table below to present the various plans in a comparable manner. Then we tried to catch the trends on factors that have been consistently emphasized, de-emphasized or are new areas of emphasis. This is a great foundation for investors to base their China portfolio on for the next five years.

Source: RVAM

Broader Societal Observations

Our broad takeaways are that there are fourteen unique focus areas across the three plans. Nine of them straddle the 14th and the 15th plan; of these only six are in the 13th plan. There is one focus area unique to the 14th plan and one unique to the 15th plan and three which were dropped after the 13th plan.

The first broad point here is that there was a much sharper change between the 13th and 14th plans compared to between the 14th and 15th plans. This is primarily due to one big reason: America and Trump. Between the writing of the 13th plan and the 14th plan, China’s view of how it sits in the world economic system and how the world views it on this same front changed dramatically. This started with the tariff policies of the first Trump term and then got re-enforced through the following years. The second point is that most focus areas have life beyond one 5-year plan. This creates a longer time horizon to make them work and hence increases their chance of succeeding. Thirdly, the CCP meets most of its targets over a long enough window, though, when it gets it wrong, the consequences are disastrous, such as the over-built property sector.

Understanding the focus areas and their implications:

- China’s 2035 Vision: This is Beijing’s long-term blueprint announced in 2020 to turn China into a “basically modern socialist country” by 2035. Strip the political speak away and it boils down to five investor-relevant goals: Tech Self-Sufficiency, High-Quality Growth (not GDP-at-all-costs), Dual Circulation Economy, Carbon Neutral Transition Track and Income Growth in tandem with Social Stability. This focus continues into the 15th plan, but was non-existent in the 13th plan.

- Quality growth more than high growth: The focus on this is the result of a combination of compulsion and choice. China’s demographic change is tectonic in terms of shrinking birth rate, total population and working age population. Birth rate numbers for 2025 that just came out are 60% below the near-term peak of 2012 and this has been a relentless drop. Consequently, the total Chinese population shrank for the third year in a row in 2025. The pre-one child policy generation (born in 1950-70s) are heading into their 60s and will hit mortality over the next 20 years leading to an accelerated drop in population. An important point is though that the working age population in China peaked in 2014 and is down 1.1% since then, Nominal USD GDP is up 90% over the same time frame. This implies a gigantic improvement in labour productivity. All this means that GDP growth can continue to come primarily from productivity improvement (quality growth) and headline growth numbers will shrink, though, like Japan, the per capita GDP growth will do better. Hence, quality rather than high growth has been the CCP’s focus area for all last three 5-year plans.

- Technological self-reliance: This started with the weaponisation of trade in technological products by the US in 2018 and continued in the subsequent years through changing administrations. This primarily focused on restricting access to semiconductor expertise and broadly covered most high-tech sectors. China quickly realised this was here to stay and dramatically increased its investment into technological expertise and capacity creation. The unassailable lead we see today in sectors like EVs, batteries, green energy, industrial machinery, consumer electronics, etc. is all a culmination of this push. Biotech, robotics, autonomous driving, AI engines, semiconductors, etc. will continue to be focus areas to expand this technological self-reliance.

- Modern industrial systems: China has come a long way from being a hub for low-cost labour being used to make shoes, clothes and toys. While it continues to do that, it has become hugely competitive on much higher value-added goods. This flows from the focus on technology, a giant market and also a relentless improvement in the manufacturing value chains. China now has over 33% of global manufacturing capacity. Hence, its export competitiveness remains high even while tariff and non-tariff trade barriers continue to grow against it from across the world. Its trade surplus, which was USD 230 bln. in 2012, has jumped to a gigantic USD 1.2 trln. in 2025. This is like a tax that the rest of the world pays to China every year and is about 1.3% of the GDP of the rest of the world. This all comes from a very strong industrial base which has been a focus area through the 13th plan and continues to be so for the current 15th plan.

- Green Transition: During the infamous January 2013 smog, AQI readings in Beijing at times exceeded 700, which is categorized as “hazardous”. Those were the days when you could actually “taste” the pollution. Today the AQI in Beijing rarely goes past 50. This is a gigantic turnaround and has not happened by chance. In 2025, 40–42% share of electricity generated in China was from low-carbon/ non-fossil sources (hydro, wind, solar, nuclear), up from 38% in 2024 and 23% in 2013. Also, currently over 50% of new four wheelers sold in China are EVs. These are all the pillars on which the environment clean up in China has occurred. Importantly, this has created a large and cheap source of renewable energy capital equipment for the world to use. Consequently, parts of the world are moving from energy shortage (with fossil fuel capacity) to energy sufficiency using renewable energy cap. For example, energy generated from fossil fuel in Pakistan moved from 67% in 2015 to 47% in 2025 – all built on Chinese products.

- Social welfare and common prosperity: This is from the focus on the spread of wealth. It is the primary difference between western capitalism and the “socialism with Chinese characteristics” of China. This leads to the kind of breakup of monopolistic businesses we saw earlier, e.g. in 2021 of the online education system in particular and the internet giants in general. China will never allow large profit pools of private capital to develop like we see in the US now. In the Chinese system, owners of financial capital are always lower in the governing hierarchy to the owners of political capital. On the other hand, in the US, the 100 richest families have a disproportionate influence over political power and seem to indirectly control it. This, for investors, creates differences and risks which are unique to China. All companies in China – public or private – have to focus on all stakeholders equally, not just primarily on the shareholders. Consequently, in China economic inequality is a lot lower than in the US and, hence there is lower public angst against the owners of capital. Remember, China is one of the only large economies in the world with zero capital gains on stock trading or on profit on sale of primary residence and has zero estate duty. This is how the CCP maintains legitimacy and it is the core of the social contract that the government has with the people in China. Going forward, expect increasing emphasis on this as social security, healthcare, pension, etc. become a larger part of the deliverables from the government.

- Deepening reforms and opening up of the economy: This has been a consistent endeavour of China since it entered the WTO in 2001. As the country became more confident in its manufacturing prowess, it has broadly opened up most industries to foreign competitors. On the services front, the opening up still lags, but the direction there too is further opening up. This creates opportunities for foreign companies. More importantly, it forces the domestic players to up their game and become more competitive in the global markets. Consequently, compared to even 10 years ago, now there are many more Chinese brands which have become global: BYD, Midea, Haier, Xiaomi, Oppo, Vivo, CATL, Sany, Geely, Miniso, PopMart are some of these global consumer brands which did not exist in any significant way ten years ago.

- Strengthening domestic demand: There was no emphasis of this point in the 13th 5-year plan, which had the primary focus on exports. Some version of this appeared for the first time in the 14th 5-year plan which started in 2021: it was called the dual circulation economy, which in plain speak means focus both on exports and domestic demand. While export went into hyper drive in this plan, domestic demand took a nose dive primarily as a fall out of the bursting of the property bubble. The 15th plan is now primarily focused on domestic demand. This is potentially the big theme for the next 5-10 years for any investor in China. As the shock from the balance sheet compression from the property sector bust slowly gets absorbed over the next 1-2 years (by then it will be a 6-year down cycle), the domestic consumer is expected to slowly come out of his protective shell. Household balance sheets remain strong and, with the government increasingly providing some version of the social safety net, we expect consumer confidence to return. This means that the potential for strong growth in consumption is high. Also, to aid this, there is a strong focus on creating wealth from financial assets (we will elaborate more on this in point 10 below).

- National security integrated with development: This is again a point that appeared in the 14th plan and did not exist in the 13th which was before Trump’s first presidency. Now it is a given that most economic decisions across countries and companies are taken with a strong focus on security of state and supply chains, geopolitics, etc. The last two 5-year plans are embedded with it. Investors in China will always have to keep this in mind.

- Reform of capital markets and financing: From the stock market perspective this is probably the most important point. It shows up for the first time in the 15th plan and had not been mentioned earlier. The focus here is to create a healthy stock market both to raise and allocate capital, and to create wealth for households and other entities invested in it. The “raise capital” part always existed but became very difficult to execute as returns from the market were anaemic for over a decade. The policy makers have only now realised that one cannot raise capital if the return on that capital is poor. The go-to investment for investors in China from 2010-2020 was property. That has clearly flipped. Property markets, even if they bottom soon, would struggle to give good returns over the medium term. Also, over 66% of Chinese household wealth is in property, and only 5-7% is in equities. Hence, the government believes that increasing returns from the stock market and thereby increasing allocation to it will repair the household balance sheet that has been damaged by the property bust. Here, as investors, we have a strong policy tailwind.

- Social and cultural advancement: This is a subtle but important focus area that was emphasized only in the 14th In layman’s terms, it meant increasing China’s soft power. It included making Chinese brands, music, entertainment, fashion, etc. cooler – though this was primarily for China, it was also focused on the rest of world. The sharp loss of market share by various global brands in China across products, price points, etc. is a sign of the Chinese consumer going more local.

- Three focus areas of the 13th plan which were subsequently dropped: These are “Urbanization and City cluster strategy”, “Sustainable Infrastructure and Connectivity” and “Poverty Alleviation and coordinated regional growth”. The first two include building infrastructure, housing, etc. – the stuff that is built with cement and steel. These are clearly the overbuilt areas, what some call white elephants or ghost buildings. This is an example of persisting too long with a very successful strategy and the result of a very slow corrective mechanism in a centralized control system. This probably should have been dropped in the 13th plan itself. The poverty alleviation was subsequently dropped as China has managed to pull a bulk of its population out of poverty and is now more of a middle-income country with a per capita GDP of about USD 14,000. This is double that of Thailand and broadly the same as that of Malaysia.

Conclusion: Focus on where the puck is going to be, not where it is

This analysis helps us to bias our portfolio towards “where the puck is going to be”. Growth in China will slow down but become more sustainable, balanced and profitable. Chinese consumers will slowly but surely become a significant force for Chinese and global growth. Tech and manufacturing expertise will move from just “best value for money” to increasingly best in class. Finally, financial market returns will be a top priority for the CCP and its leaders at all levels, thus creating a very powerful tailwind for investors. We will be looking for stocks in all these baskets.

Cover image by brgfx on Freepik

End

Disclaimer

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Information has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. Opinions and estimates constitute our judgement as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This information is directed at accredited investors and institutional investors only.