China Is Targeting Creation of Wealth Through Financial Assets

We believe that there has been a fundamental shift in a long-term trend line in China. This has been initially on the regulatory front and is now increasingly improving ground realities. The shift is the government’s focus on creating household wealth through improving returns from financial assets, especially stock market returns. This is increasingly important as the other pools of household wealth – property and bank deposits – are expected to continue to give poor returns.

This is a good starting point as current household exposure to equities is very low by historic and global standards. Also, the China market is cheap and hence a reflation there does not risk the creation of a bubble. Added to this is the regulatory impetus. This involves encouraging companies to increasingly focus on shareholder returns in terms of cash returns and improving corporate governance. There is also a clear intent to grow and nurture a larger pool of long-term permanent capital and to induce it to invest in the equity market. This includes players like pension funds, mutual funds, insurance assets, etc.

We believe this will be a very strong driver of wealth creation through strong equity market returns over the next 5-10 years. There is a group of companies which will directly benefit from this and we aim to have exposure to them.

Shift In Regulatory Focus

In September 2024, as the presidential campaign in the US engrossed the world, significant policy changes were coming out of China. Observers took note of them, promptly wrote their reports and went back to watching the US spectacle, with scant regard to the impact of the policy changes. Those path-breaking announcements had none of the fanfare and bluster of President Trump’s tariff declarations, but their impact is slowly being felt by financial markets. The stock market has started to respond, with the CSI-300 and the Hang Seng Indices having rallied by 15.7% and 25.8 % since that day.

The Chinese policymakers’ attitude to the A-share equity market has changed fundamentally since 2024. This is when they recognized that they have limited monetary or fiscal policy bazookas to make a lasting impact on the economy. The focus appears to have shifted towards anchoring up household expectations on asset prices in the stock markets first and then giving prices the impetus to grow. To achieve these goals, there have been a spate of announcements from China to stimulate the culture of financial investments and wealth creation among people, boost growth, regulate better and build guardrails, in order to make financial markets safer and less volatile and to attract long term “patient” investment capital. There has also been a concerted effort to nudge the “National Team” (key big institutions of China’s financial system) to invest directly into equity markets and to increase their allocations, especially to equities, meaningfully over time.

The First Salvo – The Two Announcements In September 2024

The two announcements out of China which stood out for their importance and wide-reaching impact over the long-term were made on September 24, 2024.

What Was Announced: Pan Gongsheng, Governor of the People’s Bank of China (PBOC), joined by officials from the National Financial Regulatory Administration (NFRA) and the China Securities Regulatory Commission (CSRC), announced a package of monetary policy measures aimed at “providing financial support for high-quality economic development”. The announcement included rate cuts, targeted support for the property sector, and two new monetary policy tools designed to stabilize the financial market. While the measures for the property sector and rate cuts were along expected lines, it is the latter two new facilities that stood out.

- PBOC credit line on financial assets: The SFISF (Securities, Fund and Insurance companies Swap Facility) was announced, the first PBOC tool explicitly targeting the stock market. Eligible securities firms, mutual funds, and insurance companies can swap less-liquid assets such as bonds, ETFs, and CSI 300 index constituents for highly liquid government bonds or central bank bills, which must then be used for stock/ ETF investments or market-making activities. The initial allocation for this facility was RMB 500bn, with potential to upsize this if required.

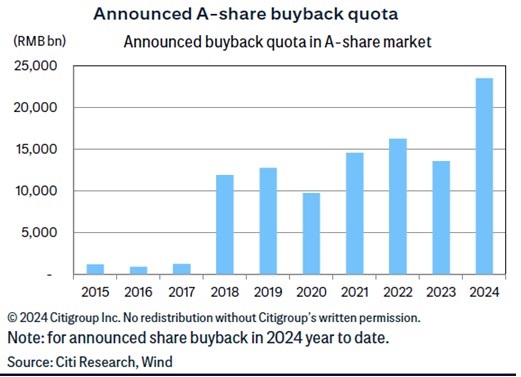

- PBOC credit line for share buybacks: The second tool was the Central Bank Lending Facility for Share Buybacks and Shareholding Increases. This facility enables banks to lend to listed companies and major shareholders exclusively for share buybacks and shareholding increases, backed by PBOC refinancing at 100% of the loan principal with an interest rate of 1.75% p.a. It provides an initial RMB 300 bn, with potential expansions to RMB 900 bn. The facility is available to all types of enterprises, including state-owned, private, and mixed-ownership entities. By late January 2025, more than 300 listed companies had disclosed their participation via this facility using more than RMB 60 bn and an average interest rate of 2% p.a.

Why It Matters: By directly engaging capital market participants, particularly investors in the stock market, these tools are meant to impact asset prices positively by stimulating both consumption and investment. Firstly, for households, it is hoped that rising asset values create a “wealth effect” and encourage spending. Secondly, for corporates, higher asset valuations improve access to capital and thus facilitate investment. By driving asset values up, it is hoped this wealth effect creates a virtuous cycle of further investments and conspicuous consumption in the economy over time, boosting growth in the economy.

Spotlight on the stock markets: China’s financial system has been dominated by bank financing, in particular through large state-owned commercial banks. By the end of 2024, RMB loans totaled 253 trn, accounting for 60% of the stock of Aggregate Financing to the Real Economy (AFRE), while corporate bonds made up 8% and domestic equity financing by non-financial enterprises was just 3%. In terms of institutional shareholdings, banks held 90% of total financial assets of all financial institutions as of Q3 2024, compared to just 3% for securities institutions and 7% for insurance companies. By putting the spotlight on the stock market and NBFIs, the PBOC appears to have decided to push for further developing the role of China’s capital markets and directing financing of the real economy through them, slowly reducing their dependance on the large banks and the banking system.

The nuanced, yet notable, takeaway from this for us is that China’s mandarins see the capital markets as serving not just the function of raising capital but, in future, to serve its investment function in a far more significant manner than at present. Their pronouncements and follow-up actions seen thus far are clearly directed towards achieving its goals of “common prosperity”.

“National Team” Takes The Lead

The “National Team” has been asked to more proactively purchase equity, both directly and indirectly via ETFs in 2024 and is doing so in 2025 as well, to limit A-share indices’ downside and to anchor market confidence.

- In January 2025, China’s State Council announced a plan to increase equity investment by the National Council for Social Security Fund (NSSF) and other pension funds as part of broader efforts to stabilize A‑share markets. Media reports indicated that in early April, the NSSF joined the so‑called “National Team” of state-affiliated investors, pledging hundreds of billions of yuan to increase A‑share exposure. No official breakdown is known as of mid‑2025 on exactly how much stock the NSSF has bought this year, either in RMB or share volumes, but we will surely know soon enough.

- Earlier, in 2024, the “National Team” including Central Huijin Investment, a unit of China’s US$1.2 trn sovereign wealth fund collectively purchased about RMB 740 bn in A‑share ETFs as part of coordinated market stabilization efforts. By end‑2024, holdings across ETFs and direct A‑shares stood at around RMB 4.1 trn, with ETF holdings alone exceeding RMB 1 trn.

- Central Huijin Investment then bought exchange-traded funds (ETFs) in April 2025 worth RMB 200 bn post the market weakness inflicted by reciprocal tariffs from the US.

- In Q1 2025, the “National Team” added substantial A‑share positions. Over 285 companies showed “National Team” as a top‑10 shareholder in their Q1 filings. Specific fund actions include the announcements in April 2025 by China Reform, Huijin, etc. of combined investments of RMB 800 bn into stocks and ETFs.

- A new regulatory mandate requires state-owned insurers to invest 30% of newly-received premiums into yuan-denominated equities from 2025 onwards. Based on 2024 premiums (~RMB 1.35 trn), projections estimate RMB 404.1 bn will flow into domestic equities in 2025 from five major insurers. Government statements targeted at least RMB 100 bn to be invested by insurers in the first half of 2025.

- The Chinese financial regulator separately authorized an additional RMB 60 bn investment from long-term insurance funds in 2025.

These are clear indications of the seriousness attached by the Chinese government to achieve their goals.

The Second Salvo

This is where the second salvo fired by the CSRC comes into play. In May 2025, the CSRC released a 25-point action plan to promote the development of mutual funds. Key measures included:

- Fee-rate reform for newly-issued active equity funds, which are encouraged to adopt performance-linked floating fee structures. Leading fund management companies must have over 60% of newly issued active equity funds meeting this requirement within one year.

- KPI reforms for mutual funds and managers in order to de-emphasize scale-related operational metrics such as fund AUMs, revenue/ earnings, etc. and prioritize return-related metrics such as NAV growth, benchmark outperformance, which must be 50% to 80% of KPI weightings in mutual fund managers’ evaluations. Managers must also co-invest in funds they manage (with a 3-year lock-up) and face substantial pay cut if their 3-year return underperforms the benchmark.

- Measures to boost mutual fund equity investments, like shorter ETF/ active equity fund registration periods. They also revamped mutual fund distributor evaluation to prioritize equity AUM retention and limit mis-selling.

Increasing Equity Exposure Of Households And Institutions – Low Starting Base

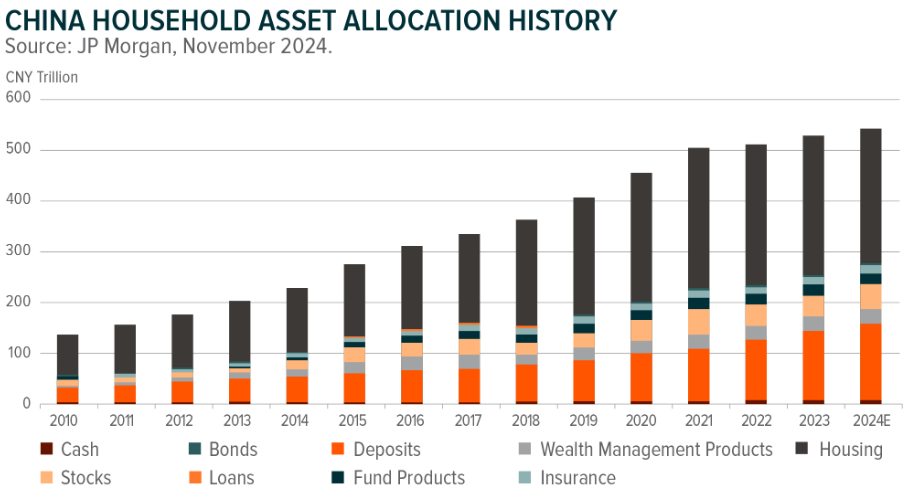

All this leads us to think of the potential impact that could be achieved over the next many years of a re-direction of capital from individuals and corporates into financial markets, including equites. To assess that, we began looking at where China’s household wealth resides.

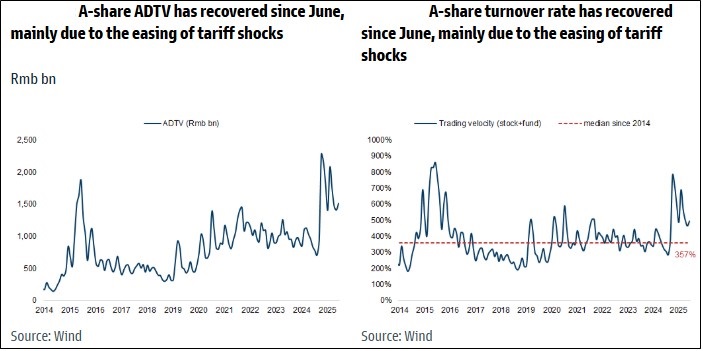

Equities’ low weight in household assets in China: In China, property (c.60%) and cash & deposits (c.25%) command the lion’s share of household assets, while equities account for just 5%, a much lower number compared to that for the US (25%), Europe (12%) and even India (7%). Post the prolonged property downturn over the past years, real estate has become a less attractive investment option. The decline in deposit rates has also disincentivized households from leaving their savings in bank deposits beyond a point. It seems logical for people to be looking towards equities to seek higher returns, which is already being reflected in stock exchanges’ average daily turnover increases, ETF growth, growth in new brokerage accounts, increase in wealth management accounts, etc.

Chinese cash sitting on the sidelines: China has the second largest pool of wealth in the world, which is invested across multiple asset classes. In 2023, China and the US contributed 17% and 25% respectively to the world’s total wealth. However, the Chinese wealth management industry encountered major setbacks due to stock market volatility and a decline in real estate values together with regulatory changes, which has led to cash hoarding in bank accounts. As a result, a mountain of cash has piled up on the sidelines, as can be seen from the accompanying chart.

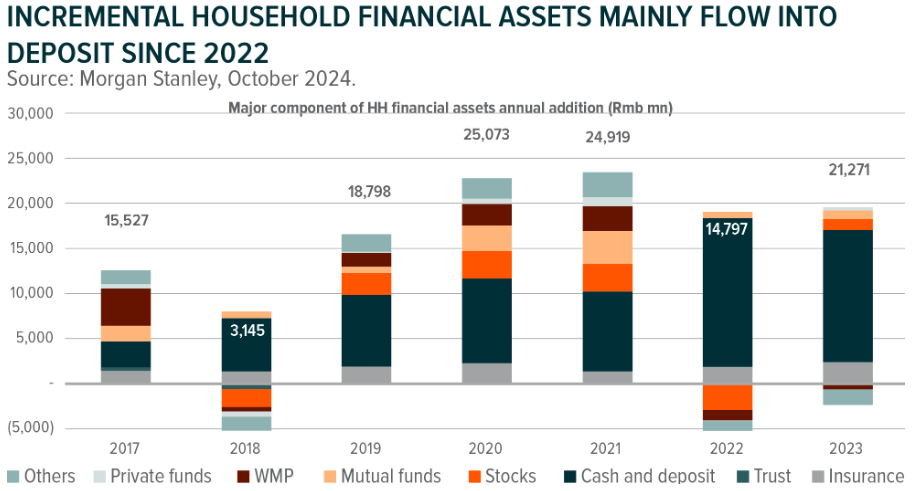

The cash hoard keeps growing: In 2022-2023, China’s household financial assets increased by ~RMB 18 trn, most of which went into deposits, with a notable shift away from equity and mutual funds’ allocations due to poor returns in the stock market.

This mountain of cash, i.e. total household deposits, had reached a whopping RMB 150 trn at the end of September 2024 and is growing further. This is larger than China’s GDP (RMB 134.9 trn in 2024) and China’s A-Share total market cap of ~RMB 90 trn.

The dark bars in the chart alongside show the overwhelmingly large inflows into cash and deposits in 2022 and 2023.

In the context of the total size of deposits in banks and the market capitalization of China’s A-share market, even a small swing out of deposits and cash into equities can have a dramatic impact on equity prices.

China’s 200 mn plus army of investors has been suffering from low returns: For Chinese investors, the property market has not been their only headache. Declining interest rates on bank deposits, guaranteed return insurance schemes and wealth management product yields, and their stock portfolios have added to their woes.

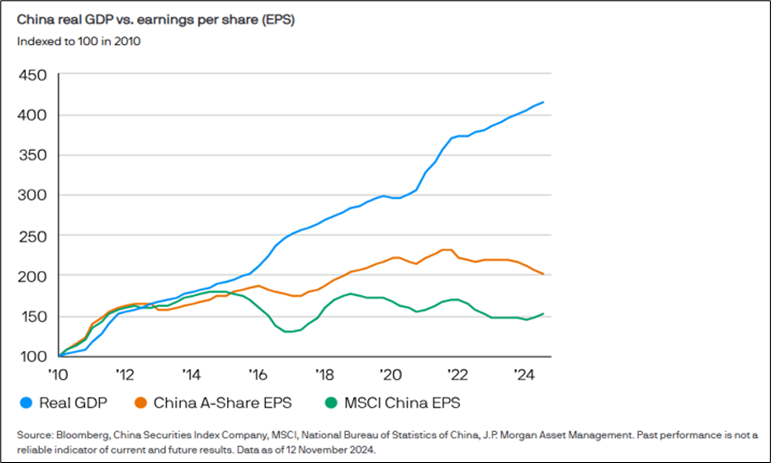

CSRC data reveals that there are more than 220 mn personal investors in China’s stock market, with an even larger number of mutual fund investors. This entire investor base has been smarting over the last few years over a deep bear market which has only begun to rise since October 2024. It is not improbable that a large number of them remain unconvinced that this rally could be a trend reversal, given the number of “false dawns” they have experienced. They cannot be blamed for their diffidence, seeing how poor China’s corporate earnings have been over the last 2-3 years (see chart alongside).

Low institutionalization is changing: China’s institutions held just 32% share of equities in Mainland China. This low institutional investment could also be because China’s A-share market is comparatively under-researched, with almost 70% of companies being covered by three or fewer analysts, according to research by Reuters. A key reason for the high market volatility in the past is attributed to the A-share markets in Shanghai and Shenzhen being dominated by retail investors, who account for an estimated 80% of market turnover. This low institutional equity presence has led to a lack of a stabilizing force during such periods.

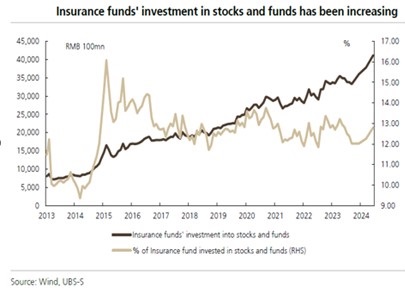

Even though the absolute quantum of funds invested into stocks has been rising as a share of total insurance funds, it remains range bound between 12-14% of the total and has potential to grow substantially in future.

However, this low institutionalization is beginning to change. Insurers and pension funds have been encouraged to step up equity investment allocation and act as anchor investors with investment KPIs shifting to focus on longer-term returns. As mentioned earlier, we saw CSRC announcing mutual fund KPI reforms in May 2025 to fundamentally change the risk reward for onshore portfolio managers to more closely track A-share equity indices, thus helping drive long-term buying flow to support the A-share market.

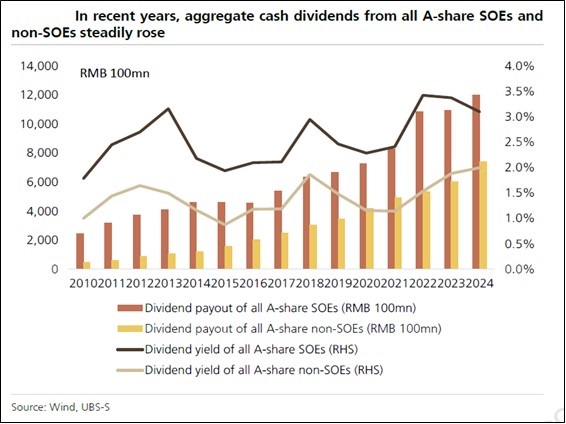

Growing cash returns from companies: In the backdrop of the still existing skepticism of the Chinese markets lies a story of rising dividends and share buybacks across SOE and non-SOE companies alike. According to an announcement by the PBOC and the CSRC in January 2025, over 300 listed companies disclosed that they used bank loans to conduct share buybacks. Further, the aggregate cash dividends of A-share list cos rose from less than RMB 300 bn in 2010 to RMB 1.93 trn in 2024, achieving a 14.4% CAGR.

Chinese Securities Companies – Strong Tail Wind With Multiple Revenue Streams

Chinese brokers and securities companies have languished for a long time, as they are seen as capital market proxies/ plays. Now that the stock markets have risen substantially off their 2024 lows, this sub-sector is getting a closer look. We have examined it closely as well.

There are several segments in the capital markets that will feel the effects of the evolving changes to regulations and the push provided by the Chinese government. These range from banks to insurance companies, asset managers, wealth management companies and non-bank financial intermediaries or securities brokers. Among these, the securities brokers are the most levered to the capital markets.

China Securities Brokers Is Where The “Puck” Is

Our current focus on the brokerage/ securities segment is premised on the wide ranging and sweeping changes occurring across the capital markets.

These brokers are typically engaged in most or all capital market activities. They either participate directly or indirectly in each of these segments across equities, fixed income, forex and currency markets and hence, depending on their individual exposure to these markets, they stand to benefit proportionately to the changes in those segments.

The securities companies typical cover the following revenue streams:

- Brokerage income: Plain vanilla retail and institutional trading, margin lending and financing and derivates trading, etc. is common to all brokers. Any increase in trading volumes and velocity of trading benefits them directly.

- Fund raising: Besides this, they also play an important role in the primary markets through IPOs, secondary issuances of companies and market making and underwriting for them. Such investment banking activities had been declining for some years now and could see a big revival starting 2025. These are additional but large sources of revenues for them. The Hong Kong IPO market has turned strongly and a 200-strong pipeline lies ahead which ought to result in all round gains for them, especially for the larger ones among them like CICC and Citic Securities, to name two.

- Wealth management: These securities firms also have their own wealth management businesses for their retail clients in China and some globally. This is a vast pool of capital that has not been tapped yet and where the re-orientation of the pools of money comes into play.

- Asset management: They also have stakes or own large and often separately listed asset management companies which are engaged in active management of funds for retail and institutional investors, and also run ETFs and hybrid funds.

- Bond underwriting: These companies are also active and large players in bonds trading and underwriting, both of which have contributed substantially to their growth in the last two to three years as interest rates declined in China.

- Market making and proprietary trading: However, the largest part of several such companies over the last five years has ended up being their large proprietary trading income or investment income. The share of this has grown while traditional sources of revenue such as brokerage income and investment banking have declined.

Investment income is also an opaque agglomeration of income whose break-up is not disclosed. Companies usually ascribe several revenue streams from trading, market making in fixed income, commodities and currencies (FICC) and interest income and capital gains on their own investment books across these. Brokers will also benefit from the changes and improvements being witnessed in the following areas.

Investment Banking benefitting from the recovery in the Hong Kong and Mainland China capital markets: The gradual recovery of the Hong Kong IPO market will boost brokers’ performance. They will also benefit if companies with ADRs return to list in Hong Kong. While limited disclosure of investment banking revenue by Chinese brokers, such as A-share and other market equity financing revenue, prevents accurate revenue estimates, GFS’s and CITICS’s investment banking revenue mainly comes from A-shares, while CICC has a larger offshore portion. CICC’s capital invested in the Hong Kong market accounts for 30% of the company’s total. Increased trading and financing activity in the Hong Kong market will benefit CICC more. We believe improved trading and financing activity in the Hong Kong market will boost brokers’ revenue growth.

Mutual Funds and ETFs AUMs starting to grow off a low base: Mutual funds and the ETF industry are seeing greater traction as new products are launched and investors begin to see the value in them and are beginning to allocate long term capital there. ETFs could become a supporting platform for brokers to develop their wealth management business. With the acceleration of passive investments, brokers could make gains in fund sales.

WM business contributes 11% to 57% of total revenue at international investment banks. However, the mix is low at China brokers. In 2023, financial products distribution was just ~4% of total revenue for the sector, which could grow to 9-10% by 2030, as per DBS.

The mutual fund net asset was RMB 31.6 trn as of December 2024, +15% yoy growth, mainly driven by the money market funds, bond funds and ETFs. The ETF net assets at RMB 3.8 trn at the end of December 2024 (+80%+ yoy), accounted for 12% of the overall MF Net Assets, which itself was a 4% growth in the same period. Following the reduction of active fund management fees in 2023, many existing ETFs in 2024 have had their management fees reduced from 0.5% to 0.15%. China’s asset management business still lags well behind overseas peers.

China’s ETF AUM remains small compared with overseas markets, implying more room for growth. China’s ETFs held less than 3% of the A-share float vis-à-vis 12.45%/ 7.7% in the US/ Japan of their respective markets.

Wealth Management seeing a reset and fresh growth: While traditional wealth management products have always been around in China, they constituted substantially of low-risk products and little into equities. A growing portion of this is now being targeted towards equities by banks and insurance companies who are the biggest players here. Brokers have the wealth management businesses for retail clients they conduct themselves while also owning asset management companies which provide active and passive funds for such investors distributed by these very brokers.

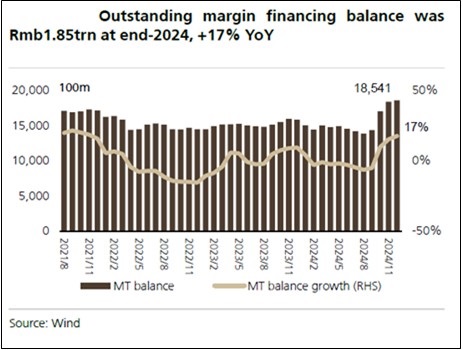

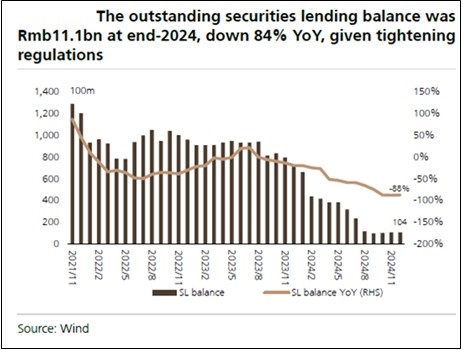

Margin financing/securities lending (MF/SL) to grow balance sheet: The retail sentiment has improved significantly since Q424, leading to the margin financing balance at year-end to be 17% higher yoy. In 2024, regulators kept a tight stance on securities lending. The SL balance at year-end was merely ~RMB 10 bn, 84% down from end-2023. However, with improvement in sentiment and market rebound, this part of the business for brokers is likely to scale up sharply in 2025 and beyond. This segment is directly corelated to the growth in the equity market participation and ties in with brokerage income from transactions and interest income for the securities industry.

The accompanying charts show that while the margin financing balance has been mostly flat for the last six odd years, the securities lending business has been crushed even from the levels seen post-Covid in 2021-22. We believe that this can grow strongly and sharply, given all the impetus to the markets, as retail investors’ participation also grows over time.

The Risks And Pitfalls For Brokers And Securities Firms’ Earnings

The obvious risk is that of the earnings recovery in China’s corporate sector, however weak and uneven, coming to a halt or going into reverse. That would cause the current rally and sentiment to be severely punctured and would lead to capital flowing out of the market. This would hurt these companies directly.

Assuming the markets trend higher over time, the brokers would surely benefit from the reasons outlined here. However, in almost every sphere of capital market activity, volumes are being countered by declining margins, spreads or yields. This is a function of the crowded nature of the market and competition as well as regulatory oversight also pushing these down. As a result, the pace of increase of revenues and profits could be moderated. Brokers who had a high exposure to bond trading benefitted in the last two years from the rally in that market. Were there to be a reversal in those markets, given the lack of market-wise disclosures, such firms could see their revenues and profits being impacted adversely.

Sector consolidation and other stock level themes will matter: While individual stock catalysts may not be present or powerful, the common sector theme at play is one of consolidation in the industry. Certain transactions have happened already and others are being talked about. However, for this to have a more direct impact on stock sentiment and valuations, we need to see more large deals being announced and consummating over the next twelve months.

Also, securities companies in China have varying exposure to the various revenue streams mentioned earlier. Some of these streams are more cyclical than others, some are more capital intensive and carry balance sheet risks, also growth rates might vary across these streams. We as investors have to be careful that we do not paint all these companies with the same brush, even though the sector level positives are common for all.

Conclusion

We believe the China securities sector is at a tipping point. In his book “The Tipping Point” Malcolm Gladwell explores how social epidemics – the rapid spread of ideas, trends, and behaviors – reach a critical mass and become widespread. He argues that small, seemingly insignificant factors can trigger dramatic shifts, like a virus reaching its “tipping point” and spreading rapidly. Several actions taken by the Chinese government have the power to influence the environment and behavior of investors that could have the same lasting effect. In China’s financial markets, the narrative of increasing volumes and participation in equity and FICC markets by domestic investors and institutions in future is a powerful one: it has stickiness and context, the two laws/ factors Gladwell deems essential for the tipping point to arrive. The biggest delta could arrive from the movement of cash on the sidelines into financial markets, regardless of asset class. This would lead to a levered virtuous cycle for these companies as operating leverage would kick in, driving profits sharply higher.

The sector trades at an average P/E of 11x and P/B 1.3x for an average RoE of 11.5%. Also, with a dividend yield of 2.5%, this is one of the few markets in the world with dividend yield higher than bank deposit rates (which stand at about 1.6% now). Combine this with the potential for corporate growth inflecting upwards, and the probability of wealth creation via financial markets in China looks high.

Cover photo by Eric Prouzet on Unsplash

End

Disclaimer

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Information has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. Opinions and estimates constitute our judgement as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This information is directed at accredited investors and institutional investors only.