We have been tracking MakeMyTrip (“MMYT”) closely for a long time. We have owned the stock before and held it during its run from the mid-thirties up toward $120. At a point late in its rise, we exited the stock.

A strong correction in the stock price started at the beginning of 2025, and we watched the stock decline over 65% the following year. We now observe it has reverted to our initial entry prices of 2024; hence, we decided to go through everything about the stock in detail once again – fundamentals, financials, competition, and the rest to understand where MMYT stands today. This is what we found:

- The business is not broken;

- Revenue is set to grow at ~20% per year;

- The company is profitable;

- It dominates every travel category in India; and

- The Indian travel story is as intact as ever.

What has changed is the price, the narrative around AI threatening platforms like this, and some real but temporary operational headwinds.

What MakeMyTrip Actually Is

MakeMyTrip operates under three brands: MakeMyTrip, Goibibo, and redBus. Together they form India’s main full-stack travel platform.

When someone books a flight or hotel through MakeMyTrip, the total value of that transaction is called the gross booking value, or GBV. This would include the total price of an airline ticket or a hotel stay. MMYT retains a slice of each booking as revenue, called the take rate. The rest goes to the airline or hotel.

The business has three main revenue streams:

- Air ticketing accounts for around 55% of GBV but only 35% of revenue; this is because margins on flights are thin (take rate around 7%);

- Hotels and packages account for 27% of bookings but 43% of revenue; this is because hotels are genuinely profitable to sell (take rate of 17 to 18%);

- Buses are the smallest but fastest growing business segment with take rates sitting somewhere in the middle.

This mix is the key to understanding where the company is going.

What Has Us Interested In MMYT?

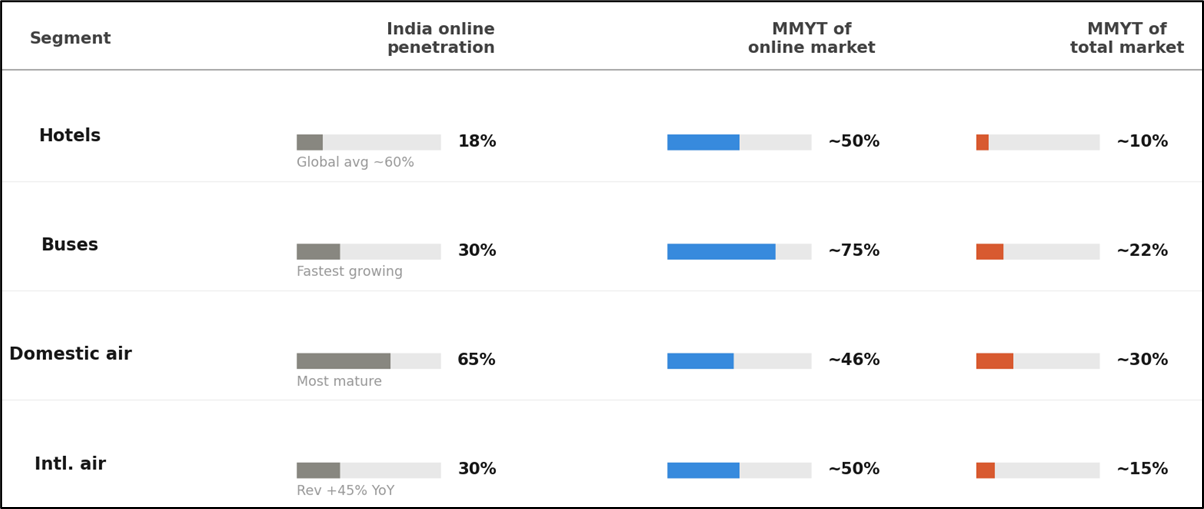

The infographic below is the whole thesis in one picture.

- The first column shows how much of each travel category in India is booked online;

- The second column shows MMYT’s share of that online market; and

- The third column shows what that implies for MMYT’s share of the total market.

Source: Company disclosures, RVAM

Let’s start with a look at the second column. Across every single category, MMYT is the dominant player in the online travel market. Roughly half of all Indians who open a travel app are on a MakeMyTrip platform. In buses, three out of four online tickets go through redBus. In hotels and international air, they have about half the online market. This is not a company competing for share, it essentially is the online marketplace.

Now have a look at the first column. Despite that dominance, the online market itself is barely developed. Only 18% of hotel stays in India are booked online, compared to 60% globally and 80% in the US. Even domestic flights, the most mature category, still have 35% of bookings happening offline. The online market that MMYT already leads is a fraction of the total travel market it could eventually own.

These two forces set MMYT up very well. Low online penetration means a long growth runway ahead, and market dominance today means there is a strong probability that MMYT will be the one capturing that growth in the online market.

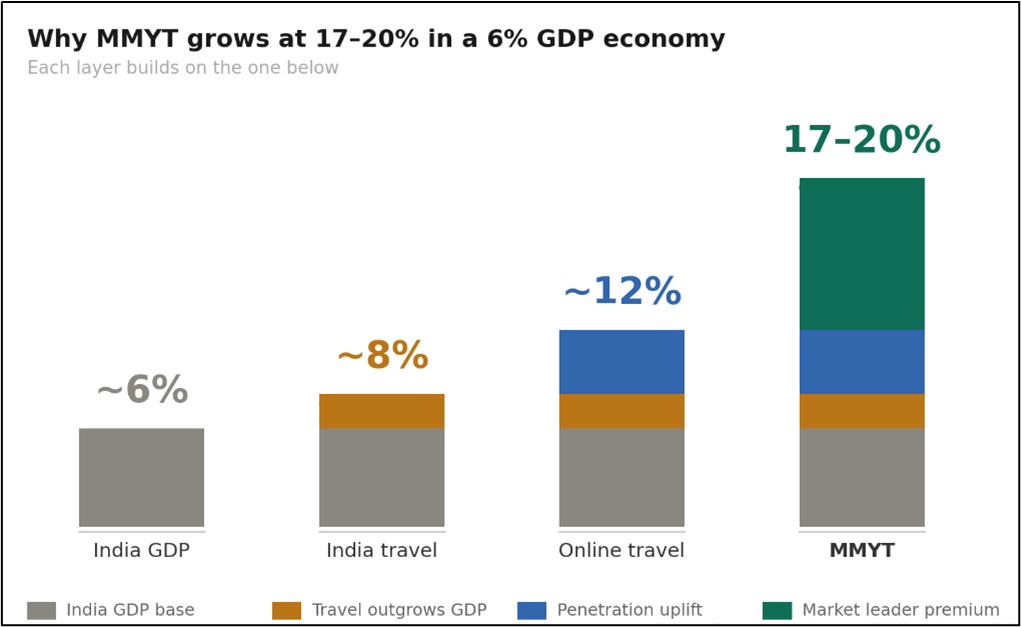

To put that growth into numbers, consider that India’s GDP grows at around 6% a year. Travel outgrows the economy by roughly 8% today, driven by rising incomes, new infrastructure, and a digitally savvy young population. Low online penetration adds another layer on top, pushing the online travel market to around 12% annual growth. MMYT, as the dominant platform in that market with no real competitor, grows faster still at 17 to 20%.

Thus, we have three compounding layers, each building on the previous one, as illustrated in the chart alongside.

Source: RVAM

The Segments You Are Not Even Paying For

When most people think about MakeMyTrip, they think about flights and hotels. That framing undersells what is actually being built.

A few years ago, buses were barely part of the story. Today, redBus is 15% of the overall business and is the fastest growing segment. India’s rapid highway expansion has transformed the category from a regional South and West India business into a national one.

The same dynamic is playing out in several other categories right now.

Holiday packages are one. The vast majority of tour and package bookings in India still happen offline. MMYT is going after this market directly by recently acquiring a majority stake in Flamingo Transworld, a major offline tours operator. They are not just waiting for the market to come to them online but are also building an offline business.

MMYT’s corporate travel has surpassed 59,000 active SME clients and 539 large enterprise accounts. Its revenues from visa services, activities and experiences, and alternative accommodations (Airbnb-style) are all small today, but they show that MMYT is expanding its business across the Indian travel market in ways that materially grow the total addressable market (TAM), which in turn gives the company an even longer growth runway ahead.

The version of MMYT that trades at $40 today is priced as a “has been” air and hotels platform. We believe that, on the contrary, neither is it a “has been” because of the young nature of the market, nor is it just an air and hotels platform.

So, why is the market beating this stock down?

The AI Question

This is one of the main reasons the stock is down, so it is worth addressing head on.

The fear is that agentic AI will just bypass travel platforms altogether. You tell your AI assistant to book a hotel room in Mumbai; it goes straight to the hotel website and books the room without MMYT in the picture. This narrative has hit Online Travel Agencies (OTAs) hard, as well as a lot of other platform and software businesses.

We think this risk is overblown, and for MMYT specifically.

Over 80% of their traffic is direct app usage. People are not finding MakeMyTrip through Google and then clicking through; instead, they open the app directly. In addition, MMYT is not sitting still. They have their own AI trip planner, they have partnered with OpenAI for various in-app uses, and they are building this on top of 25 years of data on how Indians actually travel. That is something a general-purpose model cannot replicate.

The remaining 20% that comes through search and paid channels is where the AI disintermediation argument might have some logic. But even there, when an AI routes you somewhere to complete a booking, it is more likely to send you to an OTA rather than directly to an independent hotel. OTAs have the inventory, the price comparison, the customer service. A small hotel in Goa does not have a booking infrastructure that can handle that at scale. It needs platforms like MMYT.

The AI risk for some businesses is very real, but we believe OTAs like MMYT, Booking, and Trip are likely to be less impacted by it and are also in a better position to address the risk.

There are multiple smaller but temporary reasons that have contributed to the selloff. We emphasise the word “temporary”: the Indigo incident, management delaying a margin increase, certain accounting changes, a GST change on hotel stays, and the current war in the Middle East. As these clear out, we expect the market to appreciate MMYT’s intrinsic value more than it does today.

The Financial Picture: Margin Expansion

Right now, MakeMyTrip earns an adjusted operating profit of about 1.8% of GBV. Management’s medium-term target is 2%, with the longer-term aspiration meaningfully higher.

For context, the same for Booking.com is higher than 4%. The reason is simple: over 90% of their revenue comes from hotels. Air barely features in their business.

Hotels matter most here because they are an OTA’s highest margin segment. Every hotel booking earns more than twice what a flight booking earns. As Indians move to booking more hotels online (currently sub-20% penetration), some of that volume will flow to MMYT and disproportionately improve the profitability of its overall business.

MMYT today earns about 1% on the air ticketing business and around 3% on hotels. The blended number is low because air still makes up too much of the mix. As hotels grow from 40% of revenue toward management’s long-term goal of 60-65%, that blended margin will expand naturally, without the business doing anything more aggressive. Anything they choose to do on top of that in terms of raising take rates or improving cost efficiencies will only further increase the margin.

Where Does This Put Us In Valution Terms?

If MMYT grows its gross bookings at around 17% per year through to March 2029, which we think is possible, they will have a GBV of roughly $17 billion by then. As hotels grow to a larger share and MMYT raises its take rates, the blended margin will move from 1.8% today towards around 2.7% then. That means an adjusted operating profit of around $470 million and an adjusted net profit of around $360 million by March 2029.

To put that in context, we are talking about net profit growing at roughly 40% per year for three consecutive years. That is the compounding effect of a business that is both growing its top line and improving its margins at the same time.

Now, here is where the valuation gets interesting.

Today’s market cap is roughly $4 billion and, at a net profit of $360 million in March 2029, the stock is sitting at around 11 times earnings at that point. For a company that will still be the dominant player in a young and growing market in 2029, 11 times earnings feels far too cheap. A more reasonable multiple for a business like this could be at least 20 times. At that multiple, the market cap would be about $7.2 billion and the share price around $70 with 101 million shares outstanding. That is a significant upside from where the stock is today at $40.

The additional point we find reassuring about this setup is that even if the business underperforms our expectations, there is a meaningful cushion. The stock has been beaten down so much that a lot of the bad news already appears to be priced in. Things would have to go quite wrong before an investor ends up worse off than where they are buying today.

A Catalyst That Is Not Priced In: The India Listing

MMYT has $1.4 billion of debt coming due in 2028. They currently hold around $830 million in cash. Even with the cash they will generate between now and then, covering that obligation while maintaining enough cash to run the business comfortably is a stretch.

That means they will almost certainly need to raise capital, and the most natural place to do it is India.

The company has already completed the regulatory groundwork for listing on domestic Indian exchanges, and management confirmed publicly in March 2026 that this is on the agenda.

Right now, Indian investors cannot buy MMYT as it only trades on Nasdaq. An India listing would open the door to a large pool of domestic institutional and retail capital that has been completely locked out of owning the country’s dominant travel platform. That new demand, from a motivated local investor base finally getting access, could push the valuation meaningfully higher.

Conclusion

As we continued to follow MMYT since we last sold it, we have been surprised by the extent of the selloff. The narrative around the stock had gotten quite negative between the AI fears, the slow margin progression, and the small short-term changes we mentioned earlier. But the numbers do not match the narrative at all.

The fundamentals are solid, growth is intact, the competitive position is stronger than it has ever been, and the market is still in the early stages of moving online. We are talking about a business that is arguably still in the first half of its story.

At current prices, we think we are getting a genuinely good business at a price that reflects the mood in the market rather than what the underlying company is worth.

That is why we are back.

Cover image by pikisuperstar on Freepik

End

Disclaimer

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Information has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. Opinions and estimates constitute our judgement as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This information is directed at accredited investors and institutional investors only.