It wouldn’t be outlandish to say that in recent years Singapore has become the REIT/ Business Trust capital of the East. REITs from not just within Singapore but from the U.S., Europe, China and Japan have been attracted to the SGX and listed their units here. At last count there were 44 REITs/ Business Trusts listed on the SGX of which 7 listed in the last three years alone.

For yield-seeking investors, this has created a veritable feast from which to pick and choose from. However, a listing of a REIT hasn’t guaranteed success for the sponsors as measured by the total returns delivered by their trusts. REITs, being equity-like long duration bonds, are sensitive to changes in the interest rate environment and its future outlook.

Given an environment of yo-yoing interest rates and a lower-for-longer global growth outlook, the performance of newly-listed REITs/ BTs on the SGX has been varied. We’ve been in the thick of things, trying to be early birds at spotting the ones to invest in. We seldom target just the headline yield of a newly-listed REIT. Given that it is not established yet, it is equally important to ascertain if there is potential for capital gains over the period that the REIT/BT’s undervaluation is discovered and the price appreciates. Our experience of investing in newly-listed REITs/BTs is what this month’s piece is all about.

Investors burden REIT managers with three implicit responsibilities:

- Grow distributions and hence dividend per unit (DPU)

- Own and buy assets which will appreciate and reflect through growth in Net Asset Value (NAV).

- Manage operational risks.

In the pursuit of these three objectives, a newly-listed REIT/BT has its work cut out to vie for investors’ hearts. We break down the journey of a REIT/BT into four phases, from the time it lists until the market discovers and extracts its fair value.

Post-Birth Pangs – Pregnant with Yield

Once a REIT/BT is listed it goes through a period when IPO investors and secondary markets await its first-year performance to see if it matches up to the forecast in the IPO prospectus. Through this period, broker coverage of the units is limited to perhaps one or two brokers or is often non-existent. Hence the only data investors have on which to base their judgement are the first year projected Dividend per Unit (DPU) and Net Asset Value (NAV) figures from the prospectus.

In the first year post-listing it is not uncommon to see unit prices drop below IPO prices owing to a lack of understanding of the business, the sponsor or the REIT’s prospects. This is often compounded by the desire of one or more larger cornerstone investors to sell out or reduce their stakes post-listing, accentuating the decline further. This lifts the dividend yield to mouth-watering highs, sometimes into double-digits! It is for such times that our ears are pricked. This is the period where we make the first contact with the REIT/BT.

This is also the period when the REIT/BTs liquidity is low and keeps the larger institutional investors away, even though the market capitalisation may be large enough and the yield enticing. This is usually the best time for value-cum-yield seeking investors to analyse and form an investment view on the REIT/BT. This is the period when the units would potentially be the most undervalued in absolute terms and the dividend yield at its highest.

This is also the time when the more market savvy REIT managers begin the process of engagement with sell-side analysts, directly and through the services of IR firms. Results briefings begin every quarter and brief stock reports pop up from brokers.

The First Birthday – Bash or Get Bashed!

It is not uncommon that the first birthday arrives and the units remain languishing below IPO price and well below NAV for no fault of the managers. One could blame the weak stock market trend or a downturn in the sector the REIT/BT operates in, or multiple other reasons for investors taking time to warm up to it.

The first year’s results arrive with some fanfare. The managers crow about having ‘beaten’ their projections at the investors’ meetings. Analysts feel reassured and initiate coverage around this time. The first flush of retail investors begins to arrive at the REIT/BT counter like a parched herd drawn to a watering hole sprung anew. The unit price starts to bloom like a tender sapling taking root, fertilised as it were by the fresh manna from the heavens.

The Growing Years

Seeing their new-born begin to now stride forth, the REIT management steps up the ante. Growth plans are spoken of in stronger terms to investors and analysts. They begin to showcase the REIT in the media and at roadshows at the SGX and embark on overseas trips to spread the good word to international investors. This is the period where the REIT is in the ‘buzz’ mode. The process of discovery is well and truly underway.

Some REITs/BTs announce their first acquisition within the first year of listing or soon after their first listing anniversary. It is usually from a ROFR (Right of First Refusal) from the sponsor’s portfolio of assets and will most likely be accretive to the DPU from the first year of acquisition. It may be 100% debt funded or a mix of debt (loans or notes) and equity. Equity may come usually through a rights issue or a private placement to institutional investors, depending on what P/NAV ratio the unit trades at. It usually tends to be the former unless the units are already trading above their NAV.

Notice that the unit price would be trading above or well below its NAV yet. This will determine if the REIT will be able to finance its next round of acquisitions and the financing route available to it. If the price is well below NAV, it is very likely that the REIT will not raise equity through a private placement as such an acquisition will most likely end up being dilutive to dividends. This would place a serious impediment to the growth ambitions of a REIT. However, such a REIT may yet be able to fund its first stage of growth through debt, but only to the extent of the headroom available on its balance sheet.

Post the celebrations of their first acquisition, REIT managers are put to the test to now replicate the process and bolt on more assets by the best and most efficient utilisation of the balance sheet.

Discovery – Land Ahoy!

As time elapses and if its performance remains steady and growing, the REIT gets more traction with retail and institutional investors. The unit price continues its climb further or consolidates the gains from its ‘Delivery’ and ‘Growing Years’ phases. The headline dividend yield is still attractive relative to the larger institutional REITs and hence the newly listed REIT/BT continues to attract newer classes of investors.

This is also the time by when the liquidity in the units has improved significantly enough for larger institutions to take notice. Private banks get into the act of recommending them to clients. Global investors also start to discover the REIT/BT and begin to buy in. The unit price would have reached its first major milestone of trading close to its NAV or vaulted past it.

At this stage, the REIT managers are lining up the next or first capital raise, usually a substantial one, to finance the next round of asset growth through acquisitions. Once completed successfully, the REIT has now grown to a size where more analysts and investors are attracted. The discovery of the REIT/BT in Raffles Place and Marina Bay precincts in Singapore is now complete.

Our Checklist

Our interactions and engagements involve a checklist of issues that we run through with managements. These include:

- Understand the asset class and the underlying business

- Get to know the sponsor’s background well

- Ascertain the REIT manager’s KPIs and their alignment of interests with minority

shareholders - Determine the organic growth probable within the portfolio for the next 3- 5 years

- Identify the opportunities in the medium and long term to grow assets and dividends

- Assess how much growth it can deliver without dilutions

- Determine whether dividends are fully covered by core earnings or artificially supported by

the sponsor in the first 1-2 years - Find out gearing at the REIT (the lower the better)

- Find out the cost of funding and risks associated with it

- Assess the position of the assets in the long-term asset cycle and understand the future

direction of cap. rates. This will influence NAV growth or decline.

Detailed financial analyses, projections of distribution and dividend growth follow. Once done, we’re usually ready for a first bite of the cherry!

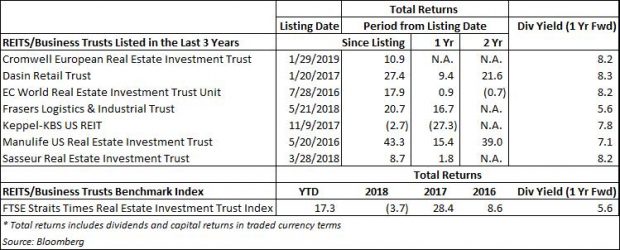

The accompanying table lists some REITs/BT’s performance since their listing from 2016 to date. The average dividend is still substantially higher than that provided by the REIT Benchmark Index.

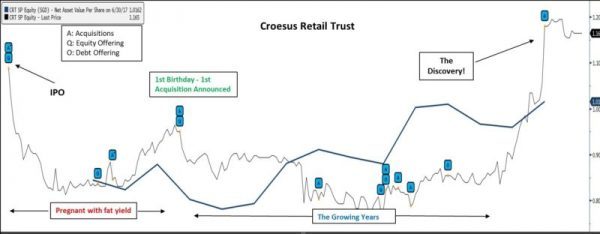

Croesus Retail Trust (CRT.SP) – Listed below its IPO price of S$0.93 in May 2013. It sold off soon after and stayed below the IPO price until Jan 2014. CRT soon executed its first acquisition followed by another soon after it announced its first-year results. Over the next few years, management executed several acquisitions funded through Debt and Equity. It received a lucrative bid for the Trust in June 2017 leading to its eventual de-listing from the SGX in October 2017.

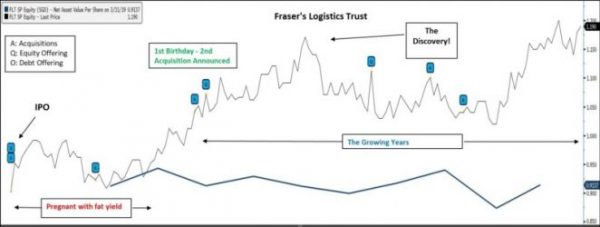

Fraser’s Logistics Trust (FLT.SP) – Given the sponsor’s strong reputation and large initial size of the Trust, FLT did not trade at a discount to NAV post-listing. Its yield was much lower than peer group post-listing. It announced acquisitions well before its first listing anniversary. This Trust should have been trading at a premium to NAV in line with some of the large Singapore logistics REITS. However it took it some time for the market to ‘discover’ its virtues. Once the acquisitions came, equity raises were done above NAV and the yield quickly compressed. FLT was fully ‘discovered’!

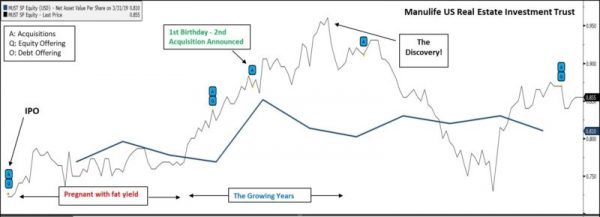

Manulife US Real Estate Investment Trust (MUST.SP) – Here was another Trust from a reputed global parent but yet it listed in May 2016 at US$0.76, below its IPO price of US$0.83. Thereafter the stock traded in a narrow range between US$0.74-0.80. The first acquisition came one year after listing in June 2017, followed by another in Sept 2017. The Discovery of the stock coincided with the period of growth for the Trust.

To conclude, at RVAM, REITs form an important constituent of the ‘yield’ basket of our equity portfolio. This component has delivered a total return of 53.5% in U.S. dollar terms in the last five years, including dividends and currency effects. In the future too we continue to seek investment opportunities in this space by sticking with our strategy to be patient and driven by our desire to own REITs operating in business segments where we have a positive view on growth rather than being merely seduced by the lure of high headline yields.

End

Disclaimer

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Information has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. Opinions and estimates constitute our judgement as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This information is directed at accredited investors and institutional investors only.