We wrote a monthly thought piece in May 2019 titled “We are all Japanese Now”. This primarily dealt with the fact that, like Japan, interest rates globally were heading towards zero. The COVID-19 crisis and the corresponding huge printing of money across the world has accelerated this trend at warp speed. The question is no more whether we are heading towards this zero-rate world, but “now what?”

This Zero-Rate World

This trend, especially for investors in markets outside of Japan (and, in the last few years, Europe), was one of those things that happened to other people. It was like some exotic disease or the winning of a lottery; these things are only read about in newspapers and never happen to you or even your acquaintances. But now it is hitting home.

Recently a social organisation that I am a part of in Singapore wanted to renew its fixed deposit with a bank. The bank shockingly offered 0% for a 2-year deposit, and then magnanimously increased it to 0.1%. This was an awakening that zero rates had arrived in Singapore (at least for corporate deposits). It would be reasonable to assume that this is an experience across markets and countries. Even in countries like India where nominal rates remain positive, the sticker shock is high when five-year bank deposits renew at rates which could be down 3-4% since the last renewal five years ago.

There is no appreciation of risk-averse savers. They are being told: either take no returns or take more risk. The scary scenario is not just a zero-rate world but the potential of a genuinely large negative rate world.

Harvard professor Kenneth Rogoff makes an interesting point. He says:

“For those who viewed negative interest rates as a bridge too far for central banks, it might be time to think again. Right now, in the United States, the Federal Reserve – supported both implicitly and explicitly by the Treasury – is on track to backstop virtually every private, state, and city credit in the economy. Many other governments have felt compelled to take similar steps.

…..(such) blanket debt guarantees are a great device if one believes that recent market stress was just a short-term liquidity crunch, soon to be alleviated by a strong sustained post-COVID-19 recovery. But what if the rapid recovery fails to materialize? What if, as one suspects, it takes years for the US and global economy to claw back to 2019 levels?”

He explains that the only way out of this is that credit wealth will need to be destroyed, either through crises like shorter and very painful write-downs of liabilities or a longer-term penalty in terms of negative return to creditors. Given the political push back against the former, the most likely scenario is long drawn zero/negative nominal and real rates.

“…wealth will be destroyed on a catastrophic scale, and policymakers will need to find a way to ensure that, at least in some cases, creditors take part of the hit, a process that will play out over years of negotiation and litigation.

…(the other option is that) the Fed could push most short-term interest rates across the economy to near or below zero. Europe and Japan already have tiptoed into negative rate territory. Suppose central banks pushed back against today’s flight into government debt by going further, cutting short-term policy rates to, say, -3% or lower.”

Source: Bloomberg

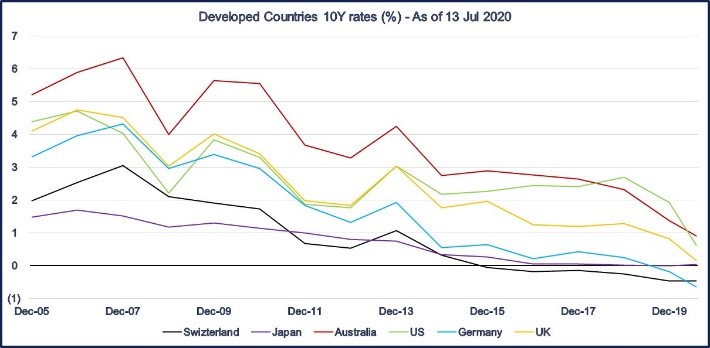

Why Do Zero Rates Sustain For So Long?

Japan’s 1-year government bonds touched 0% yield in 2005 and except for a brief period from 2006-09 when it went up to 0.5%, it has mostly been near zero and below zero since 2015. Japan’s 1-year rates were last above 1% in 1996 – 24 years ago. German 1-year rates have been negative since 2014 and 10-year rates went below zero in early 2019. Switzerland 1-year rates have also been negative since 2014, with 10-year rates broadly below zero since early 2015. The point being made here is that once low rates are reached, they can become entrenched and very difficult to get off.

The question is “why”. The broad answer is in a concept propounded by Richard Koo, Chief Economist at Nomura Research Institute. This is the concept of “Balance Sheet Recession”. He states:

- Low rates and high leverage come together: Low rates are always reached at a time when the balance sheet is highly levered. Central banks tend to keep lowering rates to postpone the painful effects of deleveraging. By then growth has long run out of sustainable drivers like improvement in productivity and better demographics. Hence leveraging up has to be used to sustain this growth. This is where we are now in most parts of the world.

- High leverage and slow growth lead to a balance sheet recession: The next step in this is that when rates reach zero and cannot go down much further, growth stalls. This leads to a society-wide desire to deleverage. At that point all surplus capital that is generated (by households, corporates and sometimes even governments) is not simply spent but just used to pay back debt. At that point even though debt is at zero cost people prefer paying back rather than spending it. This lower spending leads to a further slowdown in economic activity and hence in GDP growth. This vicious spiral is what Richard Koo refers to as “The Balance Sheet Recession”.

- The only way out of this – other than a sharp financial and credit crisis – is slow long drawn low growth environment as the loan is slowly paid back. Emerging countries can – if they have the wherewithal – carry out productivity improving structural changes. But for developed countries the most likely path is that of Japan – slow growth and low rates for a prolonged period of time.

How Do We Invest In Such An Environment?

This environment is going to last for longer than the investment time horizon of most investors. Hence a new paradigm will emerge. This will have the following salient features:

- Growth will remain low: Most economies will struggle to improve productivity or increase their labour force. Also, the ability to further increase leverage will be peaking out. Hence growth will be sparse and only in some pockets.

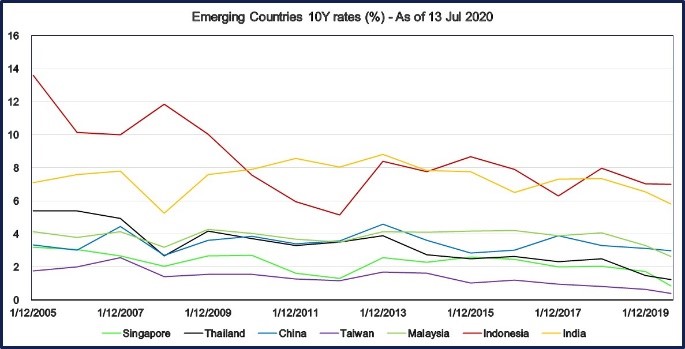

- Emerging Markets will have the opportunity of a generation: Countries with upside in terms of labour productivity and a younger demography will have a great opportunity to attract capital. Also, such markets tend to be higher nominal interest rate markets. Hence the drop in interest rates could give a significant boost to growth. Countries like India and Indonesia are prime examples of such markets. The catch is whether their leadership has the ability to execute a multi-decade process of structural reforms to unleash this potential.

- Pockets of growth will get very overvalued: This is already happening. But as we come out the current crisis, the over valuation will spread from the usual suspects (like tech) to any country, industry or stock which shows a structural growth trend.

- Hunt for yield will continue: This will be a continuous process where yield that is reliable will get consistently bid up. The way some of the businesses handle the COVID-19 crisis will determine the resilience of their growth and yield. Hence the true biding up will fully show up by the end of next year.

End

Disclaimer

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Information has been obtained from sources believed to be reliable. However, neither its accuracy and completeness, nor the opinions based thereon are guaranteed. Opinions and estimates constitute our judgement as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This information is directed at accredited investors and institutional investors only.